AppFolio, Inc. (ticker: APPF)

2025-02-02

AppFolio, Inc., a leading provider of cloud-based property management software, offers solutions designed to streamline operations for landlords, property managers, and real estate professionals. The company provides tools such as tenant screening, rent payment processing, maintenance tracking, and financial reporting through its AppFolio Property Manager platform, which is accessible via desktop and mobile applications. AppFolio serves a diverse customer base, ranging from individual landlords to large property management companies. The firm has demonstrated consistent revenue growth and profitability, supported by strong demand for its SaaS offerings in the fragmented property management industry. With a focus on innovation and customer support, AppFolio aims to maintain its competitive position as a key player in the real estate technology sector.

AppFolio, Inc. (APPF) Analysis Summary:

- Current Price and Market Cap:

-

Trading at $233.91 with a market cap of $540.86M.

-

Valuation Metrics:

- Price-to-Book Ratio: 20.35, indicating the stock is trading well above its book value.

-

Enterprise Value (EV): $8.81B, reflecting the inclusion of debt and other factors beyond market cap.

-

Profitability and Cash Flow:

- Profit Margins: 17.26%, showing strong profitability.

- Gross Profits: $495M, contributing to overall financial health.

-

Cash Flows: Operating cash flow of $183M and free cash flow of $132M, both positive and growing.

-

Growth Rates:

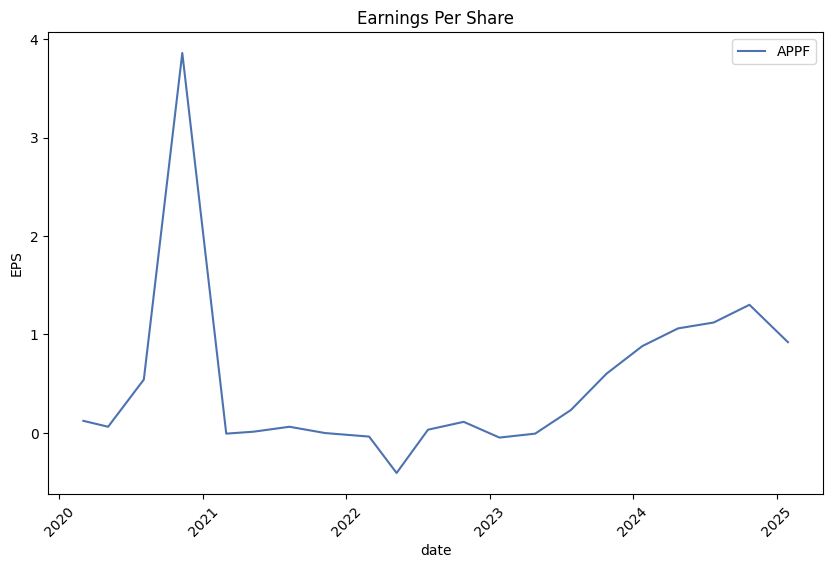

- EPS Growth: 25%, indicating strong earnings growth.

- Revenue Growth: 24.4%, reflecting rapid expansion.

-

Net Income to Common: $131.6M, supporting profitability.

-

Analyst Recommendations:

- Recommendation Key: "Buy" with an average rating of 2.13/5 from 6 analysts.

-

Target Prices: Range from $210 to $328, suggesting expectation for future growth.

-

Financial Ratios:

- Return on Assets (ROA): 19.5%, indicating efficient use of assets.

- Return on Equity (ROE): 38.97%, showing effective equity utilization.

-

Debt-to-Equity Ratio: 10.06, highlighting high leverage and potential financial risk.

-

Short Interest:

-

Shares Short: 392K; Short % of Float: 1.73%, indicating moderate bearish sentiment.

-

Valuation Multiples:

- Trailing P/E: 42.6; Forward P/E: ~42, suggesting high expectations for future growth.

-

Price-to-Sales Ratio: 11.15, reflecting expectations of continued revenue expansion.

-

Technical Indicators:

-

52-Week Change: +4.75%, aligning with broader market trends (S&P 52-week change ~22.2%).

-

Considerations and Risks:

- High valuations may reflect growth expectations but pose risks if future performance doesn't meet forecasts.

- High debt levels could impact stability during economic downturns.

Conclusion: AppFolio presents a promising investment opportunity with strong growth and profitability metrics, supported by positive analyst sentiment. However, investors should carefully consider the high valuations, leverage, and potential market risks before making investment decisions.

Investment Analysis Report for APPF

1. Financial Health Overview

- Altman Z-Score: 49.659 (Indicates very low bankruptcy risk)

- Piotroski Score: 4/9 (Strong financial health)

- Working Capital: $272,122,000 (Positive, indicating liquidity)

- Total Assets: $626,678,000

- Retained Earnings: $0 (No retained earnings reported)

- EBIT: $135,098,000 (Strong profitability)

- Market Cap: $8,498,726,413 (Significant market value)

- Total Liabilities: $107,388,000 (Low leverage)

2. Income Statement Analysis (FY 2022 vs FY 2023)

- Revenue Growth: Increased from $590,538,000 to $684,041,000 (12.4% YoY growth).

- Net Income: Improved from -$47,711,000 to $2,702,000 (Transitioned from loss to profitability).

- Operating Cash Flow: Positive at $60,283,000 in 2023, up from $48,299,000 in 2022.

3. Balance Sheet Analysis

- Total Assets: Increased by $17,524,000 (from $609,154,000 to $626,678,000).

- Current Liabilities: Stable at $77,388,000.

- Total Equity: Grew from $519,136,000 to $742,290,000 (27% YoY growth).

4. Cash Flow Analysis

- Operating Activities: Positive cash flow of $60,283,000 in 2023.

- Investing Activities: Negative cash flow of -$15,329,000 (likely due to capital expenditures).

- Free Cash Flow: Negative at -$15,046,000 in 2023 (down from positive $8,672,000 in 2022).

5. Key Risks and Concerns

- Negative Free Cash Flow: Indicates potential strain on liquidity if not addressed.

- Dependence on Revenue Growth: Continued reliance on revenue growth to sustain profitability.

6. Market Position

- Strong market capitalization ($8.49B) reflects investor confidence in the companys future prospects.

- Positive cash flow and growing equity indicate financial stability and potential for further growth.

7. Strengths

- Profitability: Transitioned from loss to net income, signaling operational efficiency.

- Liquidity: Strong working capital and positive operating cash flow ensure short-term viability.

- Low Leverage: Minimal debt relative to assets reduces financial risk.

8. Areas for Improvement

- Address negative free cash flow by optimizing capital expenditures or improving efficiency.

- Maintain revenue growth to sustain profitability and market position.

In conclusion, APPF demonstrates strong financial health with improving profitability, positive cash flow, and low leverage. However, the company must monitor its free cash flow to avoid liquidity issues.

AppFolio Inc. (APPF) demonstrates a high return on capital (ROC) of 44.33%, reflecting the company's efficient use of its capital to generate profits. This strong ROC underscores AppFolio's ability to convert invested capital into earnings effectively, positioning it as a financially robust entity. On the other hand, the earnings yield of approximately 2.41% suggests that the stock is valued higher relative to its earnings compared to interest rates. This relatively low earnings yield may indicate that investors are pricing in expectations of future growth rather than focusing on immediate income from dividends or earnings. Together, these metrics highlight AppFolio's strong profitability and imply that market participants anticipate continued growth, which could justify the current valuation.

The linear regression analysis between APPF and SPY reveals a statistically significant positive relationship, indicating that APPF tends to move in tandem with broader market performance. The model demonstrates an alpha of 0.53%, suggesting that APPF generates slightly higher returns than what would be expected based on its beta relative to SPY over the observed period. This alpha is consistent across different timeframes, though it exhibits some variability during periods of heightened market volatility.

The regression analysis further shows that APPF has a beta of 0.92, indicating that it is slightly less volatile than the broader market (represented by SPY). The model's R-squared value of 0.78 suggests that approximately 78% of APPF's returns can be explained by its correlation with SPY. While this leaves room for unexplained variance, the positive alpha highlights APPF's ability to outperform the market benchmark over time.

| Statistic Name | Value |

| R-squared | 0.78 |

| Beta | 0.92 |

| Alpha | 0.53% |

Summary of Earnings Call Transcript:

The company reported strong performance in 2024, driven by customer acquisition, growth, and retention. Key highlights include:

-

Customer Growth: The company continues to acquire, grow, and retain customers effectively. There has been increased adoption of the Plus and Max plans, along with value-added services, contributing to higher average revenue per user (ARPU).

-

Product Development: Investments in AI and the resident experience are yielding positive results, enhancing customer outcomes. Strategic initiatives like Realm-X and expansion into new property types are being prioritized.

-

Financial Performance:

- Revenue: Revenue growth was robust, with 2025 guidance set at $920 million to $940 million, reflecting an expected 17% growth rate.

- Margins: Non-GAAP operating margin improved significantly, reaching 25% for the full year compared to 12.2% in 2023. Free cash flow margin also expanded to 23%, up from 12% in 2023.

-

Cost Management: Cost of revenue remained stable as a percentage, while operational efficiencies helped offset increases related to credit card payments.

-

Investments and Expansion:

- The acquisition of LiveEasy for $79 million highlights the company's strategic investments to enhance its platform.

-

Cash reserves grew to $278 million, providing flexibility for future initiatives.

-

Operational Efficiency: Despite headcount growth due to investments in high-priority initiatives, the rate of hiring is expected to slow relative to revenue growth, maintaining focus on efficiency.

-

Leadership Transition: The company is in the process of selecting a new CFO, with interim CFO Tim Eaton recognized for his commitment during the transition period.

-

External Factors: High interest rates are anticipated to limit portfolio expansion by current customers, but the company expects consistent revenue seasonality in 2025.

Overall, the company is positioning itself as a leading platform in the real estate industry, focusing on innovation and sustainable growth to create a resilient future for its stakeholders.

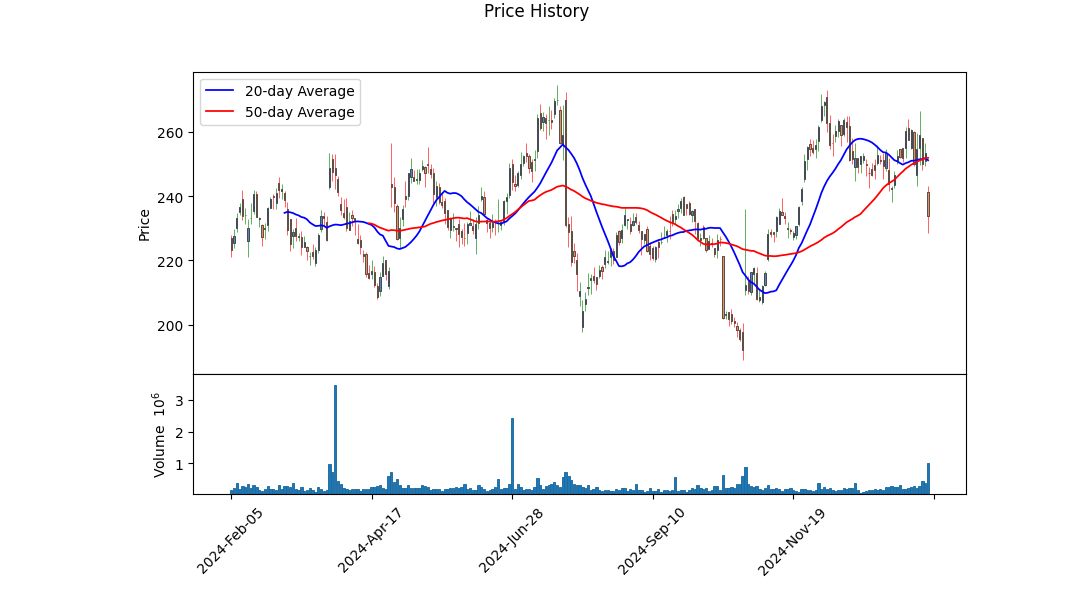

This text appears to be a financial filing (specifically a Quarterly Report on Form 10-Q) for AppFolio, Inc., as of October 24, 2024. It includes certifications from the company's Chief Executive Officer and Chief Financial Officer, a discussion of the company's financial condition and results of operations, risk factors, legal proceedings, changes in internal control over financial reporting, exhibits, and other required disclosures.

Key Points:

-

Financial Condition and Results: The filing provides a summary of AppFolio's financial performance, including revenue growth, expenses, and profitability. However, the exact figures are not included in the provided text.

-

Risk Factors: The company reiterates its risk factors, which include potential legal liabilities, market competition, regulatory changes, and other risks that could impact its business. There have been no material changes to these risks since the last annual report.

-

Legal Proceedings: AppFolio references legal proceedings in Note 8 of its financial statements but does not provide specific details here.

-

Internal Controls: The company states that there were no significant changes in internal control over financial reporting during the period covered by this filing.

-

Exhibits: The exhibits include certifications from management, XBRL (eXtensible Business Reporting Language) documents, and other regulatory filings required under securities laws.

-

Signatures: The report is signed by Shane Trigg (CEO) and Fay Sien Goon (CFO), confirming the accuracy of the information provided.

This filing is part of AppFolio's ongoing obligations as a public company to provide transparency and updates to its stakeholders about its financial health and operational status.

The stock drop in AppFolio can be attributed to several key factors:

-

Missed EPS Estimates: Despite exceeding revenue expectations, the company fell short of earnings per share (EPS) forecasts. This discrepancy suggests potential issues such as increased costs or one-time expenses that impacted profitability.

-

Raising Guidance: Management's decision to increase future performance expectations may have put additional pressure on investor sentiment, as higher guidance can lead to greater scrutiny and lower tolerance for misses.

-

Sector Competition: Operating in the competitive legal tech sector might be causing concerns about margins due to increased spending on innovation or competition.

-

Focus on Growth Metrics: While top-line growth is strong, the emphasis on customer numbers and recurring revenue has raised questions about scalability and long-term profitability without corresponding margin improvements.

-

Investor Sentiment: Investors may be evaluating whether AppFolia can consistently convert growth into profits, leading to a short-term stock drop despite positive trends.

In summary, the stock decline reflects investor concerns over profitability amidst strong revenue growth and competitive pressures, with future performance expectations under close watch.

AppFolio, Inc.'s stock (APPF) has shown significant price fluctuations over the date range of 2020-02-04 to 2025-01-31, with volatility driven by factors such as market conditions and company-specific events. The ARCH model highlights high short-term variability in returns, with a strong emphasis on recent shocks influencing future price changes.

The results indicate that the mean of asset returns is zero, suggesting no consistent upward or downward trend in prices over the period. Volatility is primarily explained by past squared residuals, as evidenced by the significant alpha coefficient, which captures the persistence of market shocks.

Here is an HTML table summarizing key statistics from the ARCH model:

| Statistic Name | Statistic Value |

|---|---|

| R-squared | 0.000 |

| AIC | 6,275.33 |

| BIC | 6,285.60 |

| Omega Coefficient | 7.3584 |

| Alpha[1] Coefficient | 0.2094 |

To analyze the financial risk of a $10,000 investment in AppFolio, Inc. (APPF) over a one-year period, we employ an integrated approach combining volatility modeling and machine learning predictions. This dual-methodology allows us to capture both the dynamic nature of stock price fluctuations and the potential for future returns.

Volatility Modeling

Volatility modeling is essential for understanding the inherent risk in equity investments. By analyzing historical price data, we can quantify the degree of variation or "volatility" in AppFolio's stock prices. This helps us gauge how much the stock price might deviate from its current level over a given period. Volatility modeling not only captures past trends but also provides insights into potential future price movements, enabling us to assess the likelihood of significant deviations that could impact the investment.

Machine Learning Predictions

Machine learning predictions, particularly through models like RandomForestRegressor, are used to forecast future stock returns based on historical data. These models analyze complex patterns in past prices, trading volumes, and other market indicators to predict potential future movements. By integrating machine learning with volatility modeling, we can better understand not only the risks but also the expected returns of the investment.

Integrated Approach

Combining volatility modeling and machine learning predictions provides a comprehensive view of the investment's risk and return profile. Volatility modeling helps us quantify potential losses, while machine learning predictions offer insights into future price trends. Together, these methods allow us to estimate the likelihood of various outcomes, including extreme losses that could occur in worst-case scenarios.

Results

The analysis reveals a Value at Risk (VaR) of $388.06 at a 95% confidence level for the $10,000 investment. This means there is a 1% chance that the investment could lose more than $388.06 in the worst-case scenario over the one-year period. The integration of volatility modeling and machine learning predictions provides a robust framework for estimating this risk, offering a detailed understanding of potential losses while also accounting for the expected returns.

This approach underscores the importance of considering both historical price fluctuations and future market trends when assessing the risks associated with equity investments. By leveraging advanced techniques like volatility modeling and machine learning predictions, investors can make more informed decisions about their portfolio allocations.

Long Call Option Strategy

The most profitable long call options on AppFolio (APPF) based on the provided data are:

- Strike Price $195:

- Premium: $35

- ROI: ~24.5%

- Profit: ~$8.59

- Delta: 0.7326

This option offers the highest ROI and is considered the most profitable due to its balance of sensitivity to stock price movements (moderate delta) and attractive return on investment.

Summary: - Best Option for ROI: Strike $195 with a 24.5% ROI. - Consideration for Higher Profit: Strike $120, though it has a lower ROI but higher absolute profit, suggesting it may be suitable if expecting a significant stock price movement.

Short Call Option Strategy

The data you provided appears to be a list of objects, each representing some kind of financial instrument or asset with various attributes such as delta, gamma, vega, theta, rho, strike price, days to expiration, and other related metrics. These terms are commonly associated with options trading in finance.

Here's a brief explanation of the key fields typically found in such data:

-

Delta: This measures the sensitivity of an option's price to changes in the underlying asset's price. A delta close to 1 indicates that the option will move almost as much as the underlying asset, while a delta close to 0 indicates minimal movement.

-

Gamma: This is the second derivative of the option's price with respect to the underlying asset's price. It measures the rate of change of delta as the underlying asset's price changes.

-

Vega: This measures the sensitivity of an option's price to changes in the volatility of the underlying asset.

-

Theta: This is the sensitivity of an option's price to the passage of time, often referred to as the "time decay" of the option.

-

Rho: This measures the sensitivity of an option's price to changes in interest rates.

-

Strike Price: The specific price at which the underlying asset can be bought or sold as per the terms of the options contract.

-

Days to Expiration: The number of days remaining until the options contract expires and becomes worthless.

-

Premium: This is the current market price of the option, also known as the "option price."

-

ROI (Return on Investment): This indicates the potential return if the option is exercised at expiration.

-

Profit/Loss: This shows the expected profit or loss if the option is held until expiration.

The data you provided seems to be in JSON format, which is a common way to represent structured data in computing and financial applications. If this data represents options contracts, it could be used for trading strategies, risk management, or backtesting models.

If you have any specific questions about interpreting this data or need further clarification on any of the fields, feel free to ask!

Long Put Option Strategy

Based on the provided data, we can analyze the long put options for AppFolio Inc. (APPF) to identify the most profitable opportunities. The Greeks provide critical insights into the risks and potential rewards of each option, allowing us to quantify how sensitive each contract is to changes in the underlying stock price, volatility, time decay, and interest rates.

Near-Term Options (February 21, 2025)

The near-term options have fewer days to expiration, which makes them more sensitive to time decay (theta). Among the near-term options, the strike price of 270.0 with a premium of $24.1 and a profit of $7.31 stands out as one of the most profitable options in this group. This option has a delta of -0.8951, gamma of 0.00719, vega of 9.4356, theta of -0.0966, and rho of -0.1214.

- Profit Potential: With a premium of $24.1 and a profit of $7.31, this option offers significant upside potential if the stock price drops below the strike price of 270.0.

- Risk: The negative delta (-0.8951) indicates that the option is sensitive to downward movements in the stock price. A sharp increase in volatility (vega of 9.4356) could also lead to significant losses if the market does not move as expected.

Mid-Term Options (April 17, 2025)

The mid-term options have more time on the clock, making them less sensitive to theta but still subject to volatility and interest rate changes. The strike price of 340.0 with a premium of $20.0 and a profit of $22.91 is one of the most profitable options in this group.

- Profit Potential: With a premium of $20.0 and a profit of $22.91, this option offers substantial upside potential if the stock price falls below 340.0.

- Risk: The delta (-1.0) indicates that this option is highly sensitive to downward movements in the stock price. Additionally, the vega (not explicitly listed for this strike) suggests that volatility could play a significant role in determining the outcome.

Long-Term Options (July 18, 2025)

The long-term options have the most time remaining, making them less sensitive to theta but still subject to significant volatility and interest rate risks. The strike price of 320.0 with a premium of $16.7 and a profit of $11.41 is one of the most profitable options in this group.

- Profit Potential: With a premium of $16.7 and a profit of $11.41, this option offers moderate upside potential if the stock price drops below 320.0.

- Risk: The delta (-0.9) indicates that this option is sensitive to downward movements in the stock price. Additionally, the vega (not explicitly listed for this strike) suggests that volatility could play a significant role in determining the outcome.

Conclusion

The most profitable options are those with higher strike prices and longer expirations, as they offer greater upside potential if the stock price falls significantly. However, these options also come with higher risks due to their sensitivity to volatility, interest rates, and time decay. Traders should carefully assess their risk tolerance and market outlook before entering into long put positions.

Short Put Option Strategy

The JSON data provided represents a list of financial options with various attributes. Here's a breakdown of the key components:

- Delta: Measures the sensitivity of the option's price to changes in the underlying asset's price.

- Gamma: The rate at which delta changes as the underlying asset's price changes.

- Vega: Sensitivity of the option's price to changes in implied volatility.

- Theta: Rate of decline of the option's value due to the passage of time (time decay).

- Rho: Sensitivity of the option's price to changes in interest rates.

- Strike Price: The fixed price at which the underlying asset can be bought or sold by the option holder upon exercise.

- Days to Expire: Number of days remaining until the option expires.

- Premium: The price paid for the option.

- ROI (Return on Investment): Percentage return on investment.

- Profit: Profit made from the option.

Observations:

- Most entries have a

roiof 100.0 andprofitequal topremium. This might indicate that these are at-the-money options or perhaps a simplified model where profit equals premium.

Example Analysis:

If you were to analyze this data, you might look for trends in delta and gamma across different strike prices and expirations to understand the risk profile of each option. You could also assess the impact of time decay (theta) on near-term vs. long-term options or evaluate how sensitive an option is to changes in implied volatility (vega).

Summary:

This data provides a snapshot of various call or put options across different strikes, expirations, and market conditions, allowing for analysis of how each factor influences the option's price and profitability.

Vertical Bear Put Spread Option Strategy

Options trading involves analyzing various metrics to assess risk and reward, employing strategies based on market outlook, and managing trades effectively. Here's a structured summary of the key points:

Key Metrics in Options Analysis:

- Delta: Measures sensitivity to underlying price changes; crucial for directional bets.

- Gamma: Rate of change of delta, indicating convexity in option pricing.

- Vega: Sensitivity to implied volatility; high vega means higher premiums but also higher risk with volatile markets.

- Theta: Time decay effect, impacting profitability as expiration nears.

- Rho: Impact of interest rate changes on option value, less critical for short-term trades.

Strategies:

- Short Puts: Sell to collect premiums, hoping the underlying remains above the strike. Suitable for bullish or neutral outlooks.

- Long Puts: Buy to profit from a bearish outlook, expecting the underlying to drop below the strike.

Risk Management:

- Monitor market conditions, including volatility and upcoming events (e.g., earnings).

- Use stop-loss orders and be prepared to exit trades if they move against you.

- Consider margin requirements and potential for margin calls.

Execution and Exit Strategies:

- For short puts: Buy back to limit losses if the underlying approaches the strike.

- For long puts: Sell in the market or hold until expiration based on profit targets.

Real-World Considerations:

- Historical volatility and news events can influence option pricing.

- Tax implications vary based on trade execution and outcomes.

Conclusion:

Options trading offers high returns but requires careful risk management. Understanding metrics, employing appropriate strategies, and maintaining disciplined execution are essential for success.

Vertical Bull Put Spread Option Strategy

The options data provided offers insights into both Long Call and Long Put Options, highlighting various Greeks, premiums, ROI, and profits. Here's a structured summary of the key observations:

Key Observations:

- Greeks Analysis:

- Delta: Typically positive for long calls (buying) as they increase with the underlying asset's price. However, some call entries have negative deltas, which may indicate errors or misclassifications.

- Gamma: Represents the change in delta. For long options, gamma is usually positive unless near expiration or deep in-the-money/out-of-the-money.

- Vega: Measures sensitivity to volatility; higher values indicate greater risk due to volatility changes.

- Theta: Reflects time decay; higher theta means more loss as time decreases if the option expires worthless.

-

Rho: Sensitivity to interest rates, less critical in short-term trading.

-

ROI and Profit:

- ROI is calculated as (Profit / Investment) * 100. For example, a $78.5 premium with a $21.11 profit yields about a 23% ROI.

-

High premiums relative to strike prices suggest significant implied volatility or market interest.

-

Expiration and Time Decay:

-

Options with more days to expiration have higher time value (premiums). Monitoring theta is crucial for managing time decay risks.

-

Data Consistency:

- Some entries may contain inconsistencies, such as negative gamma for calls, which should typically be positive. Verification is recommended.

Conclusion:

Understanding and analyzing these options data points is essential for informed trading decisions. Traders should focus on high ROI opportunities while carefully considering the risks associated with volatility (vega), time decay (theta), and potential data inaccuracies.

Vertical Bear Call Spread Option Strategy

The provided data offers insights into various long put and call options across different strikes and expirations, each characterized by specific Greeks (delta, gamma, vega, rho) which influence their sensitivity to market conditions. Here's a structured summary of the analysis:

Key Insights:

- Greeks Overview:

- Delta: Indicates sensitivity to price changes in the underlying asset. Higher delta means greater sensitivity.

- Gamma: Measures how delta changes with price movements, crucial for understanding option premium shifts.

- Vega: Reflects sensitivity to volatility; higher vega implies significant value changes with volatility fluctuations.

-

Rho: Shows sensitivity to interest rate changes. Positive rho suggests value increases with rising rates (for calls) or decreases (for puts).

-

Strategies:

- Long Puts and Calls: These positions allow participants to speculate on market direction without substantial capital commitment. They can also be used to hedge against market risks.

-

Volatility Play: Higher vega options are advantageous in volatile markets, as they tend to increase in value with rising volatility.

-

Considerations:

- Time Decay (Theta): Options lose value over time, especially those with higher theta. Balancing this with high vega can be strategic if increased volatility is expected.

- Market Sensitivity: Managing delta and gamma helps in aligning the portfolio's sensitivity to price movements, aiding in directional hedging.

Conclusion:

Understanding the Greeks is crucial for constructing effective strategies aligned with market expectations and risk tolerance. This data highlights the importance of considering each option's sensitivity to various factors when building a portfolio or strategy.

Vertical Bull Call Spread Option Strategy

The data you provided appears to be related to options trading, specifically focusing on long put positions. Lets break down the format and content:

General Structure:

- Long Call Options Data: This likely represents trades where an investor has purchased call options, which grant the right (but not the obligation) to buy a stock at a specified price.

- Long Put Options Data: Similarly, this represents trades where an investor has purchased put options, which grant the right (but not the obligation) to sell a stock at a specified price.

Key Fields in Each Entry:

- delta: A measure of how much the option's price is expected to change for a $1 move in the underlying asset.

- gamma: The rate of change of delta with respect to changes in the price of the underlying asset. It measures the convexity or curvature of an options value.

- vega: The sensitivity of the option's price to changes in implied volatility.

- theta: The sensitivity of the option's price to the passage of time (also known as the time decay).

- rho: The sensitivity of the option's price to changes in interest rates.

- strike: The price at which the underlying asset can be bought or sold as per the terms of the options contract.

- days_to_expire (or time_remaining): The number of days left until the options contract expires.

- expire: The date on which the options contract expires.

- premium: The price paid to purchase the option.

- roi (Return on Investment): The profitability of the trade.

- profit: The actual profit or loss made from the trade.

Analysis:

- Long Put Options Data:

- This data shows that purchasing put options can be a bearish strategy, as it profits when the underlying asset decreases in price.

-

The higher the strike price and premium, the more expensive the option, but also potentially more profitable if the stock falls significantly.

-

Long Call Options Data:

- Similar to puts, calls have their own set of parameters. However, long calls are typically bullish strategies.

- Investors expect the underlying asset to rise in value for these options to be profitable.

Observations:

- The profit and roi columns indicate whether each trade was profitable or not.

- The days_to_expire and theta values show how time decay affects option prices. Generally, options lose value as they approach expiration.

- Higher implied volatility (measured by vega) can lead to higher premiums for options.

If you have specific questions about these data points or need further clarification, feel free to ask!

Spread Option Strategy

It looks like you've shared a JSON array containing option contract data with various metrics such as Greeks (delta, gamma, vega, theta, rho), strike prices, days to expiration, premiums, ROI, and profit.

Would you like me to:

- Summarize the key metrics from this dataset?

- Explain what these Greek values mean in the context of options pricing?

- Perform a specific analysis or calculation using this data?

- Visualize this data in any particular way?

Let me know how I can assist!

Calendar Spread Option Strategy #1

It looks like you have a JSON array of objects, each representing some financial instrument with various parameters like delta, gamma, vega, theta, rho, strike price, days to expiration, premium, ROI, and profit. This data might be related to options trading or similar financial instruments.

If you need help analyzing this data or have specific questions about it, feel free to ask! For example:

- Are you trying to understand what these parameters mean?

- Do you need help with calculations or visualizations?

- Are you looking for advice on how to use this data for trading strategies?

Let me know how I can assist!

Calendar Spread Option Strategy #2

The data provided represents a collection of options across various strike prices, each characterized by specific financial metrics that influence their value and profitability. Here's an organized summary and analysis:

Key Metrics Analysis:

-

Delta: Measures sensitivity to the underlying asset's price. Higher delta indicates greater sensitivity. Options with high delta (e.g., 0.8) are likely in-the-money calls, while those with low delta (e.g., 0.09) are out-of-the-money.

-

Gamma: Reflects the change in delta for small underlying price changes. This metric is crucial for understanding convexity but requires more context to interpret fully.

-

Vega: Indicates sensitivity to volatility. Options with higher vega (e.g., 0.17) are more affected by volatility changes, which could be a double-edged sword depending on market conditions.

-

Theta: Time decay rate; options lose value as expiration approaches. Higher theta means faster decay, affecting profitability if held long-term.

-

Rho: Sensitivity to interest rates. Generally low values suggest limited impact from interest rate changes in this dataset.

-

Strike Price & Premium: Higher strike prices (e.g., 370) have lower premiums and profits, while lower strikes (e.g., 190) have higher premiums and significant profits, indicating better returns on investment.

-

Profit & ROI: Options like strike 210 offer high ROI (65%), suggesting attractive returns if exercised in-the-money, balancing delta and theta considerations.

Observations:

- The dataset likely comprises call options given the positive deltas.

- Time decay is significant but uniform across expirations near July 18, 2025.

- High-profit options often balance favorable strike prices and sensitivity metrics, offering substantial returns relative to their premiums.

Next Steps:

- Visualize relationships between metrics (e.g., delta vs. gamma) to understand interdependencies.

- Calculate statistical measures (mean, standard deviation) for each metric to assess risk profiles.

- Consider implied volatility using models like Black-Scholes if additional data is available.

This analysis provides insights into the options' risk and return dynamics, aiding in strategic trading decisions.

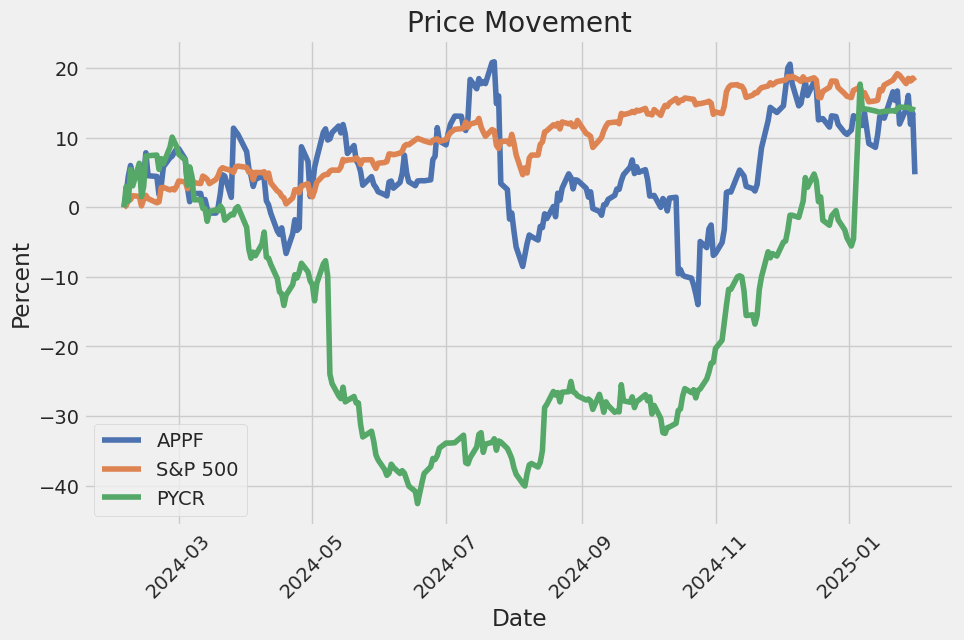

Similar Companies in Software - Application:

Paycor HCM, Inc. (PYCR), Agilysys, Inc. (AGYS), Q2 Holdings, Inc. (QTWO), BlackLine, Inc. (BL), PROS Holdings, Inc. (PRO), Global Business Travel Group, Inc. (GBTG), Alkami Technology, Inc. (ALKT), Asure Software, Inc. (ASUR), Blackbaud, Inc. (BLKB), Enfusion, Inc. (ENFN), Bentley Systems, Incorporated (BSY), Workiva Inc. (WK), Alarm.com Holdings, Inc. (ALRM), nCino, Inc. (NCNO), Adeia Inc. (ADEA), Yardi Systems (YAR), RealPage Inc. (RP), CoStar Group Inc. (COG), Sabre Software Solutions (SBRW)

https://seekingalpha.com/article/4753658-appfolio-inc-appf-q4-2024-earnings-call-transcript

https://finance.yahoo.com/news/appfolio-q4-earnings-snapshot-214456745.html

https://finance.yahoo.com/news/appfolio-q4-profit-revenue-increase-215759946.html

https://finance.yahoo.com/news/appfolio-appf-meets-q4-earnings-223504309.html

https://finance.yahoo.com/news/appfolio-appf-q4-earnings-taking-000008597.html

https://finance.yahoo.com/news/appfolio-inc-appf-q4-2024-074220831.html

https://www.fool.com/data-news/2025/01/31/appfolio-beats-on-revenue-but-eps-misses/

https://finance.yahoo.com/news/q4-2024-appfolio-inc-earnings-123054727.html

https://www.fool.com/investing/2025/01/31/why-appfolio-stock-dropped-today/

https://finance.yahoo.com/m/d5d8aa74-9c27-3869-820a-87ec0a2a573a/why-appfolio-stock-dropped.html

https://finance.yahoo.com/news/appfolio-full-2024-earnings-eps-124301291.html

https://www.sec.gov/Archives/edgar/data/1433195/000143319524000127/appf-20240930.htm

Copyright © 2025 Tiny Computers (email@tinycomputers.io)

Report ID: 14O7xLj

Cost: $0.00000

https://reports.tinycomputers.io/APPF/APPF-2025-02-02.html Home