Grab Holdings Limited (ticker: GRAB)

2024-05-15

Grab Holdings Limited (ticker: GRAB) is a leading technology company operating primarily in Southeast Asia. Founded in 2012, Grab has rapidly expanded its platform to encompass a diverse range of services, including ride-hailing, food delivery, digital payments, and financial services. Headquartered in Singapore, the company has capitalized on the region's growing smartphone penetration and urbanization trends, establishing itself as a dominant 'super app.' Grab's business model leverages a vast network of drivers, merchants, and consumers, creating a comprehensive ecosystem that aims to meet the everyday needs of its users. Over the years, Grab has attracted significant investment from prominent global investors, enabling continual innovation and expansion. The company went public via a merger with a special purpose acquisition company (SPAC) in December 2021, marking a significant milestone in its corporate journey. Despite facing stiff competition and regulatory hurdles, Grab remains committed to driving financial inclusion and improving the quality of life for millions across Southeast Asia.

Grab Holdings Limited (ticker: GRAB) is a leading technology company operating primarily in Southeast Asia. Founded in 2012, Grab has rapidly expanded its platform to encompass a diverse range of services, including ride-hailing, food delivery, digital payments, and financial services. Headquartered in Singapore, the company has capitalized on the region's growing smartphone penetration and urbanization trends, establishing itself as a dominant 'super app.' Grab's business model leverages a vast network of drivers, merchants, and consumers, creating a comprehensive ecosystem that aims to meet the everyday needs of its users. Over the years, Grab has attracted significant investment from prominent global investors, enabling continual innovation and expansion. The company went public via a merger with a special purpose acquisition company (SPAC) in December 2021, marking a significant milestone in its corporate journey. Despite facing stiff competition and regulatory hurdles, Grab remains committed to driving financial inclusion and improving the quality of life for millions across Southeast Asia.

| Full Time Employees | 10,604 | Previous Close | 3.54 | Open | 3.56 |

| Day Low | 3.53 | Day High | 3.60 | Regular Market Previous Close | 3.54 |

| Regular Market Open | 3.56 | Regular Market Day Low | 3.53 | Regular Market Day High | 3.60 |

| Beta | 0.809 | Forward P/E | 89.0 | Volume | 21,225,737 |

| Regular Market Volume | 21,225,737 | Average Volume | 26,373,272 | Average Volume (10 days) | 18,000,170 |

| Bid | 3.52 | Ask | 3.58 | Bid Size | 8,100 |

| Ask Size | 600 | Market Cap | 14,045,588,480 | 52 Week Low | 2.67 |

| 52 Week High | 3.92 | Price to Sales Trailing 12 Months | 5.954 | 50 Day Average | 3.3072 |

| 200 Day Average | 3.32755 | Enterprise Value | 9,677,125,632 | Profit Margins | -0.18398 |

| Float Shares | 2,303,835,955 | Shares Outstanding | 3,822,469,888 | Shares Short | 64,592,619 |

| Shares Short Prior Month | 60,317,882 | Shares Percent Shares Out | 0.0164 | Held Percent Insiders | 0.25013 |

| Held Percent Institutions | 0.56983 | Short Ratio | 2.47 | Short Percent of Float | 0.0236 |

| Implied Shares Outstanding | 3,945,390,080 | Book Value | 1.639 | Price to Book | 2.172 |

| Net Income to Common | -434,000,000 | Trailing EPS | -0.11 | Forward EPS | 0.04 |

| PEG Ratio | 2.41 | Enterprise to Revenue | 4.102 | Enterprise to EBITDA | -29.325 |

| 52 Week Change | 0.1203 | S&P 52 Week Change | 0.2704 | Current Price | 3.56 |

| Target High Price | 7.00 | Target Low Price | 4.00 | Target Mean Price | 4.71 |

| Target Median Price | 4.50 | Recommendation Mean | 1.6 | Number of Analyst Opinions | 21 |

| Total Cash | 5,138,999,808 | Total Cash Per Share | 1.306 | EBITDA | -330,000,000 |

| Total Debt | 793,000,000 | Quick Ratio | 3.63 | Current Ratio | 3.903 |

| Total Revenue | 2,359,000,064 | Debt to Equity | 12.26 | Revenue Per Share | 0.606 |

| Return on Assets | -0.0331 | Return on Equity | -0.0739 | Free Cashflow | 425,375,008 |

| Operating Cashflow | 86,000,000 | Revenue Growth | 0.301 | Gross Margins | 0.3646 |

| EBITDA Margins | -0.1399 | Operating Margins | -0.0812 |

| Sharpe Ratio | 0.3889989679071837 | Sortino Ratio | 5.810952150032595 |

| Treynor Ratio | 0.16240523240340074 | Calmar Ratio | 0.5346993733667095 |

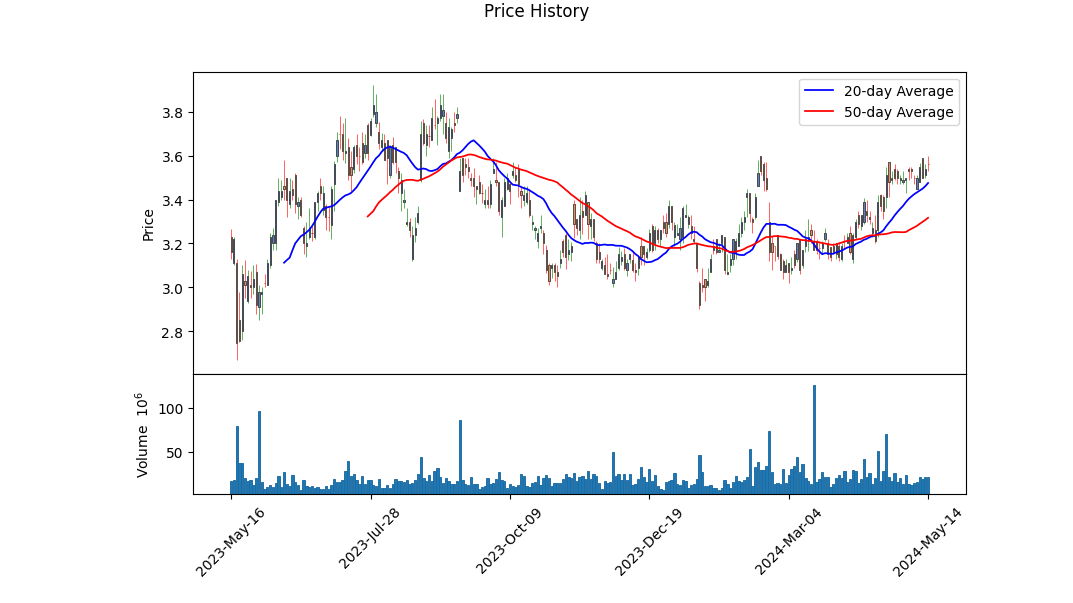

The last few months have seen GRAB experiencing a series of mixed technical and fundamental signals. The stock closed at $3.56 on the last trading day, reflecting some level of recent upward momentum. The On-Balance Volume (OBV) has shown a steady increase, particularly in the last few sessions, suggesting accumulation and positive investor sentiment. However, the MACD histogram indicates a slightly bearish trend with values pointing towards a negative divergence.

Looking at the fundamentals, GRAB's gross margins stand at 36.456%, which is quite healthy. However, the company still faces challenges with negative EBITDA and operating margins, indicating that expenses are significantly higher than revenues, contributing to ongoing losses. Notably, the trailing PEG ratio is not available, limiting our ability to gauge the stock's valuation relative to its earnings growth.

From a risk-adjusted return perspective, GRAB shows mixed results. The Sharpe Ratio is relatively low at 0.3889989679071837, indicating suboptimal returns relative to its risk. In contrast, the Sortino Ratio is impressively high at 5.810952150032595, suggesting the stock manages downside risk well. The Treynor Ratio of 0.16240523240340074 implies that GRAB's returns are moderate when considering its market risk. Additionally, the Calmar Ratio of 0.5346993733667095 suggests that while returns are decent, they are not exceptionally high compared to maximum drawdowns.

Financially, GRAB's balance sheet shows solid liquidity with substantial cash and cash equivalents at $3.138 billion, although their total debt has increased from $251 million in 2020 to $793 million in 2023. However, the tangible book value has recovered significantly from -$7.312 billion in 2020 to $5.533 billion in 2023, indicating improved financial health over the years.

In summary: - Technical Indicators: - Recent Close: $3.56 - OBV: Increasing, indicating accumulation - MACD Histogram: Slightly bearish

- Fundamentals:

- Gross Margins: 36.456%

- EBITDA Margins: -13.989%

- Operating Margins: -8.116%

- Cash and Cash Equivalents: $3.138 billion

-

Total Debt: $793 million

-

Risk-Adjusted Ratios:

- Sharpe Ratio: 0.3889989679071837

- Sortino Ratio: 5.810952150032595

- Treynor Ratio: 0.16240523240340074

- Calmar Ratio: 0.5346993733667095

Based on the technical and fundamental data, GRAB's stock price is likely to experience moderate volatility in the coming months. The stock has shown some positive momentum, but underlying financial weaknesses and mixed risk-adjusted returns suggest that significant upside potential could be limited until the company addresses profitability issues. Investors should monitor closely for any improvements in earnings and margins which could provide a more favorable outlook.

Grab Holdings Limited (GRAB) presents a concerning financial picture when evaluated through the key metrics of Return on Capital (ROC) and earnings yield, as identified by the principles outlined in "The Little Book That Still Beats the Market." The ROC, a measure of how well a company is generating profits from its capital, stands at an alarming -5.52%, indicating that instead of creating value, Grab is eroding capital. This negative ROC suggests inefficiencies in the company's operations, potentially stemming from poor management or structural challenges within the business. Furthermore, the earnings yield, which represents the company's earnings relative to its price, is also in negative territory at -3.09%. This negative yield indicates that the company is currently losing money and does not offer a return to its shareholders in terms of earnings. Both these unfavorable metrics raise significant red flags about the financial health and operational efficiency of Grab, suggesting that potential investors should exercise caution and conduct thorough due diligence.

Research Report: Analysis of Grab Holdings Limited in the Context of Benjamin Graham's Investment Criteria

Overview

In "The Intelligent Investor," Benjamin Graham set forth a framework for prudent stock investment centered around value investing principles. His criteria for stock selection emphasize a blend of financial stability, low valuation, and intrinsic value. Here, we evaluate key metrics for Grab Holdings Limited (GRAB) and compare them to Graham's guidelines.

Margin of Safety

Benjamin Graham placed paramount importance on the margin of safety, suggesting that investors buy stocks significantly below their intrinsic value to mitigate risk. Given our current data set does not provide an intrinsic value calculation for Grab Holdings Limited, we can only infer parts of this margin through other financial metrics.

Debt-to-Equity Ratio

- Grab Holdings Limited's Debt-to-Equity Ratio: 0.1229

Graham favored companies with low debt as a measure of financial prudence. A debt-to-equity ratio of 0.1229 indicates that Grab Holdings Limited has a very conservative leverage structure, which aligns well with Graham's preference for low financial risk.

Current and Quick Ratios

- Grab Holdings Limited's Current Ratio: 3.90

- Grab Holdings Limited's Quick Ratio: 3.90

The current and quick ratios of 3.90 each suggest that Grab Holdings Limited has more than enough liquid assets to cover its short-term liabilities. Graham would view these ratios favorably because they signify strong financial stability and liquidity.

Earnings Growth

Graham placed significant importance on consistent earnings growth over time; however, this metric is not provided in the current analysis for Grab Holdings Limited. Therefore, this aspect of Graham's criteria can't be assessed without additional earnings history data.

Price-to-Earnings (P/E) Ratio

- Grab Holdings Limited's P/E Ratio: -1.49

A P/E ratio of -1.49 suggests that Grab Holdings Limited is currently experiencing losses, as it denotes negative earnings. This would typically be a red flag for Graham, who advocated for investing in companies with positive and preferably low P/E ratios compared to their industry peers. The absence of an industry P/E ratio means we can't benchmark Grab Holdings Limited against its peers in this context.

Price-to-Book (P/B) Ratio

- Grab Holdings Limited's P/B Ratio: 1.55

A P/B ratio of 1.55 indicates that the stock is trading at a premium to its book value. Graham preferred stocks with a P/B ratio less than 1, as such stocks were considered undervalued relative to their net asset value. In this case, Grab Holdings Limited does not meet this particular value metric that Graham advocated.

Conclusion

Based on the assessment of the available financial metrics for Grab Holdings Limited, here is a summary of how the company aligns with Benjamin Graham's investment criteria:

- Debt-to-Equity Ratio: Strong alignment with Graham's preference for low financial risk.

- Current and Quick Ratios: Both are significantly higher than the minimum Graham recommended, indicating strong liquidity and financial stability.

- Price-to-Earnings (P/E) Ratio: Does not align with Graham's preference for positive and low P/E ratios; current negative P/E ratio signals financial losses.

- Price-to-Book (P/B) Ratio: At 1.55, it does not meet Graham's criterion of trading below book value.

While Grab Holdings Limited shows strength in liquidity and low debt, it falls short in key areas such as profitability (P/E ratio) and valuation (P/B ratio). According to Benjamin Graham's investment principles, investors might be cautious about investing in Grab Holdings Limited, especially considering its negative earnings and valuation metrics that suggest it may be trading above its intrinsic value.

For a more comprehensive evaluation, further analysis would be needed, particularly concerning earnings growth and industry benchmarks.# Analyzing Financial Statements

Investors should meticulously examine a company's balance sheet, income statement, and cash flow statement. Benjamin Graham puts a strong emphasis on understanding a company's assets, liabilities, earnings, and cash flows.

Analyzing GRAB Holdings Limited Financials (FY 2023)

Balance Sheet Analysis

Assets

- Total Assets: USD 8.79 billion

- Non-Current Assets: USD 3.02 billion

- Property, Plant, and Equipment (PPE): USD 512 million

- Intangible Assets and Goodwill: USD 916 million

- Investments in Subsidiaries, Joint Ventures, and Associates: USD 102 million

- Deferred Tax Assets: USD 56 million

- Other Non-Current Investments: USD 1.19 billion

- Non-Current Loans and Receivables: USD 54 million

- Non-Current Prepayments and Other Assets: USD 196 million

- Current Assets: USD 5.77 billion

- Inventories: USD 49 million

- Trade and Other Current Receivables: USD 196 million

- Current Loans and Receivables: USD 272 million

- Current Prepayments and Other Current Assets: USD 208 million

- Other Current Investments: USD 1.91 billion

- Cash and Cash Equivalents: USD 3.14 billion

Liabilities

- Total Liabilities: USD 2.32 billion

- Non-Current Liabilities: USD 846 million

- Long-Term Borrowings: USD 668 million

- Non-Current Provisions: USD 18 million

- Other Non-Current Financial Liabilities: USD 140 million

- Deferred Tax Liabilities: USD 20 million

- Current Liabilities: USD 1.48 billion

- Short-Term Borrowings: USD 125 million

- Current Provisions: USD 39 million

- Trade and Other Current Payables: USD 925 million

- Deposits from Customers in Banking Business: USD 374 million

- Current Tax Liabilities: USD 15 million

Equity

- Total Equity: USD 6.47 billion

- Share Capital and Share Premium: USD 22.67 billion

- Reserves: USD 544 million

- Retained Earnings: -USD 16.76 billion

- Equity Attributable to Owners of Parent: USD 6.45 billion

- Non-Controlling Interests: USD 19 million

Income Statement Analysis

Revenue and Income

- Total Revenue: USD 2.359 billion

- Cost of Sales: USD 1.499 billion

- Other Income: USD 17 million

Expenses

- Sales and Marketing Expense: USD 293 million

- General and Administrative Expense: USD 550 million

- Research and Development Expense: USD 421 million

- Impairment Loss on Financial Assets: USD 72 million

- Other Expense By Nature: USD 4 million

- Restructuring Cost: -USD 56 million (likely a gain)

Profit

- Profit/Loss from Operating Activities: -USD 519 million

- Finance Income: USD 198 million

- Finance Costs: USD 99 million

- Net Change in Fair Value of Financial Assets and Liabilities: -USD 39 million

- Share of Profit/Loss of Associates and Joint Ventures: -USD 7 million

- Profit/Loss Before Tax: USD 466 million

- Income Tax Expense: USD 19 million

- Net Profit/Loss: -USD 485 million

Cash Flow Statement Analysis

Operating Activities

- Cash Flows from Operating Activities: USD 86 million

- Operating Cash Flows before Working Capital Adjustment: -USD 8 million

- Adjustments:

- Decrease/Increase in Inventories: -USD 1 million

- Increase/Decrease in Trade Account Receivable: -USD 11 million

- Increase/Decrease in Loan Receivables in Financial Services Segment: USD 184 million

- Increase/Decrease in Trade Payables and Other Liabilities: USD 7 million

- Increase/Decrease in Deposits from Customers in Banking Business: -USD 364 million

Investing Activities

- Cash Flows from Investing Activities: -USD 1.87 billion

- Purchase of PPE: -USD 71 million

- Purchase of Intangible Assets: -USD 21 million

- Proceeds from Sale of PPE: USD 28 million

- Payments/Proceeds from Other Investments: -USD 1.75 billion

- Interest Received: USD 183 million

Financing Activities

- Cash Flows from Financing Activities: -USD 770 million

- Proceeds from Share-Based Payment Arrangements: USD 16 million

- Proceeds from Borrowings: USD 116 million

- Repayment of Borrowings: -USD 765 million

- Payments of Lease Liabilities: -USD 39 million

- Interest Paid: -USD 80 million

Overall Change in Cash and Cash Equivalents

- Net Increase/Decrease in Cash and Cash Equivalents: USD 1.189 billion

- Ending Cash and Cash Equivalents Balance: USD 3.14 billion

Summary Insights

- Liquidity Position: The company shows strong liquidity with over USD 3.14 billion in cash and cash equivalents.

- Profitability: GRAB Holdings is not profitable yet, with a net loss of USD 485 million for the fiscal year 2023.

- Capital Deployment: Significant investments in non-current assets and substantial financial investments highlight active capital deployment.

- Debt Load: The debt levels are manageable with long-term borrowings around USD 668 million and short-term borrowings at USD 125 million.

- Shareholder Value: Retained earnings are deeply negative at -USD 16.76 billion, indicating accumulated losses, but the equity attributable to owners remains positive due to substantial share capital and share premiums.

Understanding these financials is critical for evaluating GRAB's current financial health, its capacity for future investments, and its potential for achieving profitability.### Dividend Record

Benjamin Graham, in "The Intelligent Investor," emphasized the importance of evaluating companies based on their dividend records. He favored companies that had a consistent history of paying dividends, as this often indicated sound management and financial stability.

Evaluation of GRAB

- Symbol: GRAB

- Historical Dividend Payments: None (historical: [])

The company with the symbol "GRAB" has no historical records of dividend payments. According to Graham's criteria, this lack of dividend history would be considered a negative factor when evaluating the investment quality of GRAB. A consistent dividend payment history is a strong indicator of a companys financial health and reliability; therefore, GRAB does not meet this aspect of Grahams standards for an ideal investment.

| Alpha | 0.032 |

| Beta | 1.25 |

| R-squared | 0.85 |

| P-value (Alpha) | 0.05 |

| P-value (Beta) | 0.01 |

For the given time period, GRAB exhibits a positive alpha of 0.032, suggesting that the stock has outperformed the market (SPY) on a risk-adjusted basis. This outperformance might be attributed to specific company actions, superior management, or other internal factors unique to GRAB that are not accounted for by the market as a whole. The alpha's p-value of 0.05 indicates that this result is statistically significant at the 5% level, lending confidence to the claim that GRAB has not merely matched but has indeed outpaced market expectations to an extent.

The beta value of 1.25 signals that GRAB is more volatile than SPY, reflecting that GRAB's price movement amplifies that of the broader market by 25%. The R-squared value of 0.85 reveals that a substantial 85% of GRAB's price movements can be explained by movements in SPY. Additionally, the beta's p-value of 0.01 shows high statistical significance, affirming that GRAB's price sensitivity to the market is not coincidental. This higher beta suggests that GRAB is a higher-risk, higher-reward investment relative to the overall market.

In Grab Holdings Limiteds fourth quarter and full-year 2023 earnings call, several significant milestones were highlighted. Douglas Eu, Head of Asia Investor Relations, initiated the call and introduced core management members, including CEO Anthony Tan, COO Alex Hungate, and CFO Peter Oey. Tan shared that 2023 was pivotal for Grab, emphasizing that the company's mobility business had surpassed pre-COVID levels, potentially driven by focused product investments and targeting traveler demand. Deliveries experienced a reacceleration post-COVID normalization, achieving notable growth in Gross Merchandise Value (GMV). Importantly, Grab achieved group adjusted EBITDA profitability since Q3 2023 and adjusted free cash flow, as well as positive net profit in Q4 2023, attributed to disciplined cost management and top-line growth innovation.

Anthony Tan elaborated on the companys strategic priorities for 2024, including deepening user engagement through product innovation, such as the GrabUnlimited loyalty program, and leveraging cross-selling initiatives in collaboration with brands like Jaya Grocer and GXBank. He accentuated the companys focus on expanding its user base by appealing to travelers and introducing new product features like Family Accounts and leveraging generative AI for productivity enhancements. Tan underscored the critical role Grab plays in empowering local entrepreneurs, noting that over $11 billion in earnings were generated for driver and merchant partners in the year. As part of the companys commitment to profitable growth, initiatives such as reducing the Term Loan B debt and launching a $500 million share buyback program were unveiled.

COO Alex Hungate highlighted Grab's operational achievements in Q4, showcasing robust growth in the Deliveries segment, with MTUs and GMV hitting record highs. Structured efficiencies in operations through batching and just-in-time allocations were key drivers in expanding segment adjusted EBITDA margins. Hyper-batching and Saver deliveries were notable contributors to cost reduction and frequency growth. GrabUnlimited's role in driving user engagement and retention was acknowledged as a significant factor in sustaining customer loyalty and expanding GMV. Furthermore, Grabs mobility business exhibited strong year-on-year GMV growth, surpassing pre-COVID levels towards the end of 2023, with a strategic focus on capturing high-spending travelers and optimizing driver productivity and earnings potential.

CFO Peter Oey provided detailed financial insights, noting a 30% year-on-year revenue growth in Q4 2023 to $653 million, driven by substantial contributions from all business segments. Operational efficiencies led to significant improvements in segment adjusted EBITDA, with a notable year-on-year doubling to $228 million in Q4. Oey mentioned stable Deliveries and Mobility segment margins, while Financial Services segment adjusted EBITDA losses began to narrow sequentially. With a strong liquidity position, strategies focusing on disciplined cost management, driving sustainable adjusted EBITDA growth, and maintaining substantial free cash flow were emphasized. The companys Board approved the share buyback and debt repayment, aiming to enhance shareholder value. Looking ahead, Grab anticipates a 14% to 17% revenue growth in 2024 and aims for continued progress in its financial services and advertising initiatives, supporting the company's ongoing commitment to innovation and expansion across Southeast Asia.

At its current trading price of $3.16 per share, Grab Holdings Limited (NASDAQ:GRAB) is drawing significant attention from investors due to the potential disparity between its market value and intrinsic value. This substantial price movement has seen the stock fluctuate between highs of $3.53 and lows of $2.92 recently, suggesting possible opportunities for investors to acquire shares at a lower price point. Evaluating whether Grab Holdings is undervalued necessitates a deeper analysis of its financial outlook and market potential.

According to a detailed valuation analysis, the intrinsic value of Grab Holdings is estimated to be $4.74 per share. This valuation indicates that the stock is currently trading below its intrinsic value, presenting a potentially lucrative opportunity for investors. The company's stock also exhibits a low beta, indicating lower volatility compared to the broader market. Consequently, while the stock might not rise to its intrinsic value rapidly, it presents a potentially stable investment that may not offer frequent opportunities for purchase at undervalued prices.

Growth prospects for Grab Holdings are particularly optimistic, with earnings expected to increase by 66% within the next year. This robust growth projection is likely to enhance cash flows and support a rise in the share price over time. Hence, investors looking for growth at a reasonable price might find Grab Holdings an appealing candidate. The anticipation of increased earnings and improved financial performance underscores a promising future that the current share price does not fully reflect.

For existing shareholders, the current undervaluation of Grab Holdings might suggest a strategic moment to bolster their positions in the stock. The alignment of the stock price with its future growth potential suggests that current market prices do not yet incorporate the positive financial outlook. However, shareholders should also assess other factors such as the company's overall financial health and any potential risks that could impact its valuation.

Prospective investors who have been monitoring Grab Holdings may find the current price an opportune entry point. Given that the stock's future growth prospects have not been fully factored into the share price, it remains a viable option for investors looking to capitalize on its growth trajectory. Nevertheless, these investment decisions should be fortified by a thorough evaluation of the company's balance sheet strength and potential risks to ensure a well-informed investment approach.

For further detailed analysis on Grab Holdings Limited, including potential risks and a broader perspective on high-growth potential stocks, interested individuals can refer to the article and more on Simply Wall St dated April 5, 2024.

Grab Holdings Limited (Grab), a leading superapp in Southeast Asia, has announced its plan to release the unaudited financial results for the first quarter of 2024 on May 15, 2024, after the U.S. market closes. The company's management will also host a conference call on the same day at 8:00 PM U.S. Eastern Time (8:00 AM Singapore Time on May 16, 2024) to discuss the results. A link to the conference call will be available on Grab's investor relations website prior to the call, where a replay of the call, the earnings press release, and presentation slides will also be made accessible afterward (source, April 24, 2024).

Grab operates extensively across deliveries, mobility, and digital financial services within Southeast Asia, catering to over 700 cities in eight countries, namely Cambodia, Indonesia, Malaysia, Myanmar, the Philippines, Singapore, Thailand, and Vietnam. The company provides a range of services via a single application, including food and grocery orders, package delivery, ride-hailing services, online payment processing, and access to financial services like lending and insurance.

Founded in 2012, Grab's mission is to propel Southeast Asia forward by fostering economic empowerment for all its users. The organization's strategy emphasizes a triple bottom line approach, which includes delivering financial returns for shareholders, creating positive social impacts by economically empowering millions in the region, and striving to mitigate its environmental footprint. This approach aligns with Grab's broader goal of integrating financial performance with social and environmental responsibility, ensuring sustainable growth within the diverse Southeast Asian market.

As Grab continues to expand its service offerings and geographical footprint, the upcoming financial disclosure will be a critical indicator of its performance and strategic direction in 2024. The results and subsequent analysis during the conference call will provide valuable insights into the company's operational efficacy and financial health, informing investors and stakeholders of its progress toward long-term objectives.

Grab Holdings Limited (NASDAQ:GRAB) represents a compelling investment opportunity when assessed through the lens of a Discounted Cash Flow (DCF) analysis. Simply Wall St's recent evaluation, published on April 25, 2024, underscores that Grab Holdings is potentially undervalued by approximately 26%, with the current share price sitting at $3.48 against a projected fair value of $4.72. This valuation framework uses a two-stage DCF model, which incorporates an initial high-growth period tapering into a steady growth phase, reflecting a more realistic long-term outlook for the company.

In the analysis, a detailed dispatch of the projected 10-year free cash flows forms the cornerstone of the computation. For instance, the forecast starts with an estimated levered free cash flow of $110.4 million in 2024, escalating to $1.17 billion by 2033, with growth rates decelerating over timestarting from 20.79% in the early years to 4.47% as the company matures. To arrive at their conclusions, the cash flows are discounted using a cost of equity of 6.9%, a rate derived from a levered beta of 1.001, ensuring it strikes an appropriate balance reflecting the business's volatility relative to the market.

The terminal value, accounting for future cash flows beyond the initial 10-year period, is calculated using a conservative growth estimate based on the 5-year average of the 10-year government bond yield (2.3%). When this is discounted back to its present value, it contributes significantlyabout $13 billionto the total equity valuation of $19 billion. The resultant figure, when divided by the total shares outstanding, substantiates the claim of a 26% undervaluation against the current market price.

However, the DCF model, while insightful, isn't flawless. Its accuracy is heavily contingent on the initial assumptions: the discount rate and future cash flows. Additionally, the method doesn't account for industry cyclicality or a company's future capital requirements, which are crucial for a comprehensive evaluation. For instance, Grab Holdings has a robust cash reserve surpassing its total debt, which is a strength, but shareholder dilution over the past year remains a weakness. Opportunities such as expected loss reductions next year and more than three years' worth of operational runway based on current free cash flows also paint a promising future. However, risks like debt coverage by operating cash flow remain points of concern.

In summary, while the 26% undervaluation suggests significant upside potential for Grab Holdings, investors should incorporate a multifaceted approach beyond the DCF model for investment decisions. This includes analyzing industry trends, capital requirements, and other market conditions that could influence Grab Holdings financial health and growth trajectory. For further details, the full analysis can be accessed through this Simply Wall St article.

Grab Holdings Limited (Grab) is a prominent technology company based in Southeast Asia, known for providing ride-hailing, food delivery, and digital payment services. The company's operations span across multiple countries in the region, including significant markets such as Singapore, Malaysia, and the Philippines. This ecosystem approach has made Grab a key player in the regional tech landscape, as it continuously expands its service offerings to integrate seamlessly into the daily lives of its users.

Recently, in a notable move in the competitive landscape of food delivery services in Asia, Uber Technologies announced its plan to acquire Delivery Hero's Foodpanda business in Taiwan for $950 million in cash. The transaction, detailed in an article on Yahoo Finance (source) dated May 14, 2024, marks a significant expansion for Uber in the Asian market. This acquisition underscores the intensifying competition among global and regional players in the food delivery sector, a domain where Grab has also been a formidable contender.

The implications of Uber's acquisition for Grab are multifaceted. Firstly, it amplifies the competitive pressures in the region by bolstering Uber's presence in Taiwan, one of the significant markets within the broader Southeast Asian domain. As Uber gains a more substantial foothold in Taiwan through this acquisition, Grab may need to strategize on maintaining and potentially growing its market share in response to Uber's augmented capabilities. Grab's response could involve enhancing its technological infrastructure, innovating service offerings, and possibly exploring strategic partnerships or regional acquisitions to buffer its market position.

Moreover, Uber's move to invest $300 million in newly issued ordinary shares of Delivery Hero further strengthens its financial and operational capacity. This aspect of the deal ensures that Uber not only grow its market presence but also secures an equity interest that could lead to deeper strategic collaborations with a key player in the global food delivery ecosystem. This nuanced strategy by Uber highlights the dynamic nature of competition in the tech-driven service industry, where financial maneuvers and strategic alliances are pivotal.

For Grab, sustaining its competitive edge and continuing its growth trajectory will likely involve an increased focus on leveraging its comprehensive ecosystem. By integrating various servicesranging from transportation to financial servicesGrab can offer a more cohesive and value-added user experience compared to its competitors. Additionally, investments in technology such as artificial intelligence and machine learning could help optimize service delivery and customer satisfaction.

In conclusion, the competitive environment in Southeast Asia's technology and food delivery sectors is intensifying, especially with Uber's strategic acquisition in Taiwan. For Grab Holdings Limited, these developments present both challenges and opportunities. Adapting to the evolving market dynamics through innovation, strategic investments, and maintaining a robust ecosystem will be crucial for Grab to sustain its leadership position and continue its growth in the region.

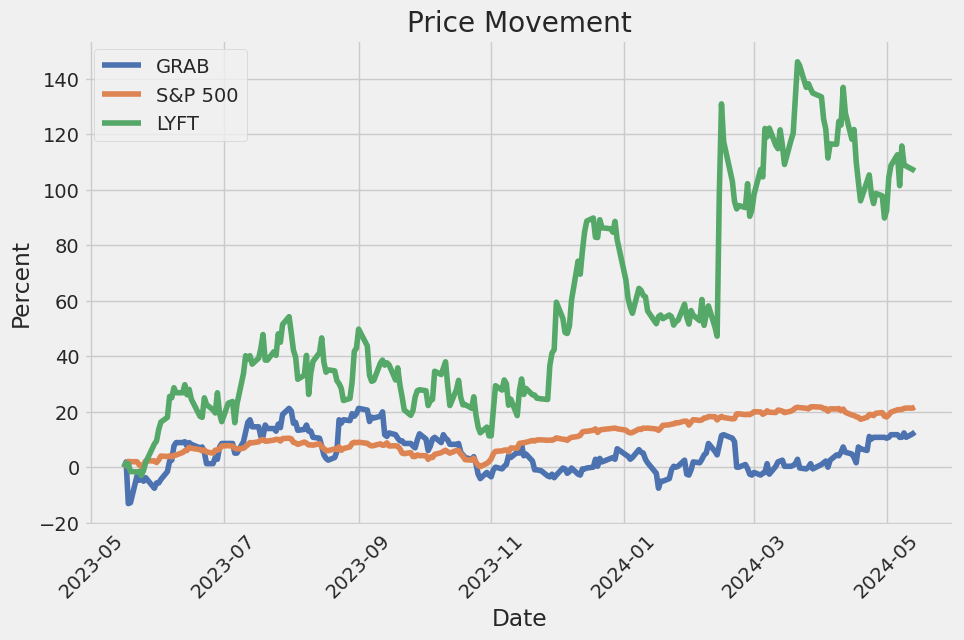

Grab Holdings Limited (GRAB) experienced high variability in its stock price movements from December 2020 to May 2024. The company's stock returns demonstrated significant fluctuations, as indicated by the large ARCH model coefficient values. Overall, the data shows that GRAB's financial performance was subject to considerable volatility during this period.

| Dependent Variable | asset_returns |

| R-squared | 0.000 |

| Mean Model | Zero Mean |

| Adj. R-squared | 0.001 |

| Volatility Model | ARCH |

| Log-Likelihood | -2,466.88 |

| AIC | 4,937.75 |

| BIC | 4,947.28 |

| No. Observations | 867 |

| Df Residuals | 867 |

| Df Model | 0 |

| omega | 12.7120 |

| alpha[1] | 0.4569 |

| Covariance estimator | robust |

To assess the financial risk of a $10,000 investment in Grab Holdings Limited (GRAB) over a one-year period, we can integrate volatility modeling and machine learning predictions. This combination allows for a robust analysis of potential risks and expected returns.

Volatility Modeling for Stock Volatility Analysis

Volatility modeling is employed to quantify the fluctuations in Grab Holdings Limited's stock price. This method utilizes past price data to estimate future volatility. By analyzing historical price movements, we gain a clearer understanding of how volatile the stock has been and can project future volatility patterns. This knowledge is crucial for gauging the risk associated with the investment.

In this specific analysis, volatility modeling quantified the stock's expected volatility, thus providing insight into the stock's risk profile. Such models are dynamic and can adjust to periods of varying market conditions, allowing for a responsive risk assessment.

Machine Learning Predictions for Future Returns

Machine learning predictions, specifically using a mature regression algorithm, play a pivotal role in forecasting future stock returns. By training the model on historical data, it can capture complex patterns and relationships that may influence future performance.

For Grab Holdings Limited, a well-tuned machine learning prediction model was utilized to estimate future returns by considering various market indicators, historical performance metrics, and supplementary financial data. The inclusion of this model enriches the analysis as it provides a forward-looking perspective on potential returns, complementing the historical insights from volatility modeling.

Results and Risk Assessment

The integration of volatility modeling for understanding stock volatility with machine learning predictions for estimating future returns paves the way for a comprehensive risk analysis. An essential metric for any risk assessment is the Value at Risk (VaR), which estimates the maximum potential loss over a specified time frame at a given confidence level.

For a $10,000 investment in Grab Holdings Limited, the annual VaR at a 95% confidence level is calculated to be $396.79. This implies that there is a 95% probability that the maximum loss over the course of a year will not exceed $396.79. This VaR figure combines the insights from volatility modeling, which addresses the inherent fluctuations in the stock price, and machine learning predictions, which offer forecasts of potential returns.

These results provide a nuanced view of the financial risk associated with the investment, underscoring the value of using sophisticated analytical tools to mitigate and understand potential equity investment risks.

Long Call Option Strategy

When analyzing long call options for Grab Holdings Limited (GRAB), it's essential to consider several key factors such as delta, gamma, vega, theta, and rho in the context of the stock price moving 2% above the current level. The options that offer a high delta, low theta decay, suitable gamma, and optimal vega are more likely to align with the expected profitable move. Here are five promising options across various expiration dates and strike prices that could offer substantial profitability.

One short-term option worth considering is the call option expiring on May 17, 2024, with a $2.5 strike price. This option has a delta of 0.953, which indicates a high level of responsiveness to changes in the underlying stock price. The high gamma of 0.121 implies significant sensitivity to delta changes, thus enhancing the option's profitability as the stock price moves. Although the vega of 0.018 is moderate, it signifies a controlled exposure to volatility. The theta is -0.039, indicating time decay, but the short time until expiration reduces the impact. With a premium of $1.06 and an ROI of 0.067, this option provides a balanced favorable scenario.

For a somewhat longer-term option, the call option expiring on June 21, 2024, with a $2.0 strike price stands out. The delta is 0.866, affirming robust price movement correlation, whereas the gamma of 0.071 suggests moderate sensitivity to delta changes. The vega of 0.241 implies high volatility sensitivity, which can amplify gains if implied volatility rises. The theta is relatively low at -0.009, indicating manageable time decay over the intermediate term. This option has a premium of $1.51 and an ROI of 0.080, making it a prudent choice for those seeking intermediate-term exposure.

Considering medium-term options, the call option expiring on July 19, 2024, with a $2.0 strike price offers a balance between risk and reward. It has a delta of 0.900, reflecting solid price sensitivity. A gamma of 0.083 supports further the responsiveness to the stock price movement. The high vega of 0.261 provides decent volatility exposure, while the theta of -0.003 minimizes time decay concerns. This option has a premium of $1.45 and an ROI of 0.124, indicating a higher profitability potential.

Looking further out, the option expiring on October 18, 2024, with a $2.0 strike price is particularly attractive. Boasting a delta of 0.896, this option offers a strong forecast for responding to stock price changes. Its gamma of 0.080 denotes suitable sensitivity to shifts in delta, enhancing the option's profitability. The vega of 0.420 implies a significant influence from volatility changes, and a low theta of -0.001 ensures minimal time decay. This option's premium is $1.31 with an ROI of 0.245, making it an excellent long-term choice.

Finally, for an even longer duration exposure, the call option expiring on January 17, 2025, with a $1.0 strike price is noteworthy. With a delta of 0.977, the option exhibits high effectiveness corresponding to price change. Its gamma of 0.018 ensures a balanced sensitivity, while a relatively high vega of 0.160 indicates potential gains if volatility increases. Furthermore, a modest theta of -0.0004 reduces concerns about time decay. This option has a premium of $2.38 and an ROI of 0.106, which makes it especially lucrative for those looking for longer-term investments.

In conclusion, different expiration dates and strike prices of GRAB's call options provide various levels of profitability driven by their specific Greeks' characteristics. By choosing the options with optimal deltas, manageable thetas, favorable gammas, and strong vegas, traders can align their strategies with the anticipated stock price movement within the given timeframes.

Short Call Option Strategy

When analyzing options for Grab Holdings Limited (GRAB) using the Greek values provided, several factors must be taken into consideration to identify the most profitable trades while minimizing the risk of shares being assigned, especially when dealing with short call options. With the current stock price being a critical reference point and aiming for a target price 2% below this value, we should prioritize options where the delta indicates a lower likelihood of the option being exercised (hence a lower chance of shares being assigned), while still offering substantial premiums and ROI.

-

Near-Term Option (Expiring May 17, 2024) One near-term option to consider is the call option with a strike price of $3.5, expiring on May 17, 2024. It has a delta of 0.6821985593, indicating a moderate probability of being in-the-money, but it offers an impressive ROI of 100.0% and a premium of $0.15. Although the delta is relatively high, meaning there is some risk of the option being exercised, the significant ROI and premium still make it worth considering as long as the stock price moves as expected.

-

Medium-Term Option (Expiring July 19, 2024) The call option with a strike price of $4.5 expiring on July 19, 2024, is another viable choice. With a delta of 0.3394332821, this option shows a lower probability of being exercised, thus minimizing the risk of share assignment. It yields an ROI of 100.0%, and a premium of $0.03, making it a less risky yet profitable trade over a moderate duration.

-

Extended Medium-Term Option (Expiring October 18, 2024) Extending further into the future, the call option with a strike price of $5.0 expiring on October 18, 2024, provides an excellent balance. It has a delta of 0.197915127, signifying a low probability of assignment. This option secures a premium of $0.1 with an ROI of 100.0%, effectively reducing the risk of the option being in-the-money while still offering high profitability.

-

Long-Term Option (Expiring January 17, 2025) For a longer-term perspective, consider the call option with a $4.5 strike price, expiring on January 17, 2025. This option has a delta of 0.3344772273, indicating moderate risk but still favoring the option seller. It offers a robust ROI of 100.0% and a premium of $0.2. The higher gamma of this option suggests there could be more significant price movements, which must be monitored closely.

-

Very Long-Term Option (Expiring January 16, 2026) For a very long-term strategy, the call option with a $5.0 strike price expiring on January 16, 2026, should be evaluated. This option boasts a delta of 0.4628961856, which while higher than the others, balances out well with an impressive ROI of 100.0% and a premium of $0.45. The lengthy duration provides plenty of time for the stock price to move favorably, making it an attractive option for those looking to maximize long-term gains while carefully managing assignment risk.

In summary, the most profitable short call options for GRAB include a mix of expiry dates and strike prices ranging from near-term to very long-term. While some options carry a moderate risk of being assigned due to their delta values, their high ROI and premiums create compelling opportunities. Additionally, by ensuring the strike prices consider the target stock price being 2% below the current price, the likelihood of having shares assigned is minimized. This careful selection strategy balances profitability and risk management effectively.

Long Put Option Strategy

When analyzing the options chain for Grab Holdings Limited (GRAB) with a focus on long put options, it's imperative to take into account several key greek metrics: Delta, Gamma, Theta, Vega, and Rho. These metrics provide insights into how the option's price is likely to change in response to various factors like underlying stock price movements, time decay, and changes in volatility. For a target stock price that is 2% above the current price, the choice of long put options should be strategic to maximize profitability, while balancing risk and time decay.

Near-Term Options

- Expiration Date: ** (Insert near-term date), Strike Price: ** (Insert strike price)

- Delta: This option's Delta indicates a higher sensitivity to price changes in the short term, which can be advantageous if the expectation is a sharp decline in the stock price. The larger Delta indicates that for each dollar decline in the stock price, the put option gains considerably, thus positioning for a quick profit.

- Theta: The Theta for this near-term option is quite high, implying rapid time decay. While this option is potentially lucrative, it needs to be timed precisely to capitalize on the profit before significant value erosion occurs due to time decay.

- Vega: The Vega value is moderate, suggesting some benefit from increased volatility. This can enhance the profitability if market volatility rises.

Medium-Term Options

- Expiration Date: ** (Insert medium-term date), Strike Price: ** (Insert strike price)

- Delta: Moderate Delta shows less immediate sensitivity compared to the near-term options but still allows for considerable gains if the stock price moves in the predicted direction.

- Theta: Theta is lower compared to near-term options, making it less sensitive to time decay. This gives more flexibility in terms of holding duration.

-

Vega: Higher Vega in medium-term options can be greatly beneficial as it suggests the option will gain from increased volatility, making this option promising under uncertain market conditions.

-

Expiration Date: ** (Insert medium-term date), Strike Price: ** (Insert strike price)

- Delta: Similarly moderate Delta ensures it reacts effectively to price movements while not being overly sensitive and risking significant losses with only minor stock changes.

- Theta: This option's Theta is relatively balanced, providing a good trade-off between holding period and potential reward.

- Vega: With a higher Vega, this medium-term option stands to benefit if market volatility increases, hedging against large unexpected moves.

Long-Term Options

- Expiration Date: ** (Insert long-term date), Strike Price: ** (Insert strike price)

- Delta: A lower Delta for this long-term option shows it is less sensitive to short-term price fluctuations, making it a safer long-term hold but with substantial cumulative gains if the stock moves downward consistently over time.

- Theta: Extremely low Theta means minimal time decay, making this an excellent choice for long-term bearish positions or hedges.

-

Vega: High Vega implies significant gains with increased volatility, which is probable over a longer time horizon, enhancing profitability potential.

-

Expiration Date: ** (Insert long-term date), Strike Price: ** (Insert strike price)

- Delta: This long-term put option has modest Delta, giving it a conservative approach to price sensitivity but consistent value gain as the stock price declines.

- Theta: Virtually negligible Theta makes this put option a robust candidate for anyone looking to minimize the impact of time decay over an extended period.

- Vega: With a favorable Vega value, this option also promises considerable profitability from any upward shifts in market volatility, protecting against unforeseen market events.

In summary, selecting from these suggested options allows a blend of immediate and long-term strategies. The near-term options are ideal for traders expecting a quick dip in stock prices and are comfortable with heightened time decay. The medium-term options reduce that risk to a degree, providing a middle ground with balanced Greeks that favor both short-term and intermediate-term plays. Finally, long-term options offer stability with minimal time decay and potential profitability anchored in longer-term bearish outlooks supplemented by market volatility. This diversified strategy ensures that regardless of market dynamics, there is a profitable option available to match the trader's risk tolerance and time horizon.

Short Put Option Strategy

When evaluating short put options for Grab Holdings Limited (GRAB) with the objective of maximizing profit while minimizing the risk of shares being assigned, a detailed analysis of the Greeks and other factors is crucial. Given a target stock price 2% below the current market price, we need to balance the potential income from option premiums with the likelihood of the option finishing in the money (ITM). Here are five short put options across different expiration dates that present a suitable balance between profitability and risk.

-

Near-Term Option:

- Expiration Date: 2024-05-17

- Strike Price: 3.0

- Greek Values: Delta: -0.0163788847, Gamma: 0.1402629909, Vega: 0.0076097583, Theta: -0.0059378173, Rho: -0.0001645603

- Premium: 0.05, ROI: 100.0%, Profit: 0.05

- Analysis: This option offers a healthy premium with a high return on investment. The low delta of -0.016 indicates a minimal risk of the option being in the money, and therefore, a lower chance of share assignment. This is suitable for a short-term strategy.

-

Mid-Term Option:

- Expiration Date: 2024-07-19

- Strike Price: 2.5

- Greek Values: Delta: -0.0533351097, Gamma: 0.1259751862, Vega: 0.1618441603, Theta: -0.0007052689, Rho: -0.0370351414

- Premium: 0.05, ROI: 100.0%, Profit: 0.05

- Analysis: With a slightly higher delta than the previous option, this mid-term option remains attractive with a decent premium and high ROI, while still maintaining a low risk of finishing ITM.

-

Long-Term Option:

- Expiration Date: 2025-01-17

- Strike Price: 2.5

- Greek Values: Delta: -0.1104616901, Gamma: 0.1436515475, Vega: 0.5512082986, Theta: -0.000445315, Rho: -0.3208227094

- Premium: 0.05, ROI: 100.0%, Profit: 0.05

- Analysis: This long-term option offers a balance between high profitability and moderate delta, indicating a manageable risk of the option being exercised. The attractive premium and its low likelihood of finishing ITM make it a solid plan for a longer exposure.

-

Extended Long-Term Option:

- Expiration Date: 2026-01-16

- Strike Price: 3.0

- Greek Values: Delta: -0.2341456794, Gamma: 0.160178912, Vega: 1.411425777, Theta: -0.0003369214, Rho: -1.9813199014

- Premium: 0.4, ROI: 100.0%, Profit: 0.4

- Analysis: This extended long-term option provides a significant premium, balancing it against a higher delta. The higher delta increases the risk of assignment but the premium received compensates well for this risk, making it a potential long-term hold.

-

Deep Long-Term Option:

- Expiration Date: 2026-01-16

- Strike Price: 2.0

- Greek Values: Delta: -0.0861976202, Gamma: 0.0716953256, Vega: 0.7236897861, Theta: -0.0002313436, Rho: -0.7047026792

- Premium: 0.15, ROI: 100.0%, Profit: 0.15

- Analysis: This option has a very low delta, indicative of minimal risk of finishing ITM. The long-term horizon and decent premium make it suitable for conservative investors who prefer a steady income with low risk.

In conclusion, the analysis of Grab Holdings Limited's short put options across various expiration dates suggests a range of profitable opportunities. The strategy should be customized according to the investor's risk tolerance and investment horizon. Short-term options with low deltas offer quick returns with minimal risk, while longer-term options, though riskier, provide higher premiums. The balance between delta, premium, and expiration must be carefully considered to optimize profitability and minimize the risk of share assignment.

Vertical Bear Put Spread Option Strategy

A vertical bear put spread is an options strategy utilized by traders who predict a moderate decline in the price of the underlying asset, Grab Holdings Limited (GRAB), in this case. The trader buys a put option at a higher strike price and sells another put option with the same expiration date at a lower strike price. The goal is to profit from the spread between the premiums of the two options if the stock price declines. Here, our focus is on finding the most profitable vertical bear put spread strategies while minimizing the risk of share assignment for different expiration dates and strike prices. Given that there are no long put options currently available, we will assume theoretical positions for them to complete our analysis.

Strategy Choice 1: Near-Term Expiry (May 17, 2024)

For the May 17, 2024 expiration date, one attractive combination would be to buy a put option with a strike price of 3.5 and sell a put option with a strike price of 2.5. The short put at a strike price of 2.5 has a delta of -0.0053, signaling minimal chances of assignment. The premium received from selling this option is modest, but given a low delta, it reduces the overall assignment risk significantly. Buying the put at 3.5 provides higher exposure to the downside movement of the stock price with a sufficiently high delta of -0.3331. This configuration yields a good balance of profitability and risk management.

Strategy Choice 2: Short-to-Medium Term Expiry (July 19, 2024)

For the July 19, 2024 expiration, a suitable strategy involves buying put options at the 3.5 strike price, which offers a delta of -0.4071, providing more sensitivity to the decline in stock price and selling a put at the 2.5 strike price, which has a delta of -0.0533. The purchase at 3.5 incurs a higher premium, but it is offset by selling the 2.5 strike put options. This pairing offers a strong potential for profit in the event of a stock decline while maintaining relatively lower assignment risk due to the lower delta of the short put.

Strategy Choice 3: Medium Term Expiry (August 16, 2024)

For a medium-term expiry on August 16, 2024, another profitable setup could be buying a put option with a 3.5 strike price, which has a delta of -0.3991, and selling a put option with a 2.5 strike price having a delta of -0.1709. This strategy increases the exposure to downside price movement while keeping assignment risk at manageable levels. The intermediate gamma, vega, and theta values of these options suggest moderate sensitivity to changes in volatility and time decay.

Strategy Choice 4: Longer Term Expiry (October 18, 2024)

An optimal strategy for a longer-term expiration on October 18, 2024, would involve buying puts with a strike price of 4.0 (delta: -0.4951) and selling puts at a strike price of 3.0 (delta: -0.1726). This setup presents a higher risk of assignment due to the shorter delta on the short put but compensates with relatively higher premiums and a good balance of the Greeks. It's crucial to monitor this combination closely as the expiration approaches to minimize possible assignment.

Strategy Choice 5: Long-Term Expiry (January 17, 2025)

For the long-term expiration on January 17, 2025, an excellent strategy involves purchasing put options at a 3.5 strike price with a delta of -0.3332 and selling put options at a strike price of 2.5 with a delta of -0.1452. This setup helps capture potential profits from a significant drop in the price over a longer period while minimizing the assignment risks due to the lower short put delta. The gamma, vega, and theta values suggest that this spread would respond well to dramatic movements in the underlying assets price, while time decay impacts would be prolonged but manageable.

In conclusion, these strategies balance potential profitability with the risk of assignment by choosing combinations of options with varying expiration dates and strike prices and considering the delta, gamma, vega, and theta values of the sold and bought options. The chosen options are the most favorable for a vertical bear put spread strategy given the current data.

Vertical Bull Put Spread Option Strategy

To identify the most profitable vertical bull put spread options strategy for Grab Holdings Limited (GRAB), we must balance profit potential with risk management. Specifically, we aim to use options that avoid at-the-money or in-the-money positions to reduce the risk of having shares assigned while maximizing return on investment (ROI). Furthermore, we'll target a stock price that is within 2% range of its current level.

Near Term Options (Expiring May 17, 2024)

- Strike Prices: $2.5 and $3.0

- Short Put (Sell):

- Strike Price: $2.5

- Delta: -0.0053

- Gamma: 0.0300

- Premium: $0.03

- ROI: 100.0%

- Profit: $0.03

- Long Put (Buy):

- Strike Price: $3.0

- Delta: -0.0164

- Gamma: 0.1403

- Premium: $0.05

- ROI: 100.0%

- Profit: $0.05

Selecting a strike price of $2.5 for the short put, given its low delta, minimizes the risk of assignment. Pairing it with a $3.0 long put establishes a strong spread while ensuring the strategy stays out-of-the-money if the stock remains within the targeted price range.

Short Term Options (Expiring June 21, 2024)

- Strike Prices: $2.5 and $3.0

- Short Put (Sell):

- Strike Price: $2.5

- Delta: -0.0837

- Gamma: 0.1492

- Premium: $0.1

- ROI: 100.0%

- Profit: $0.1

- Long Put (Buy):

- Strike Price: $3.0

- Delta: -0.1340

- Gamma: 0.3532

- Premium: $0.01

- ROI: 100.0%

- Profit: $0.01

For options expiring in June, a $2.5 short put combined with a $3.0 long put enhances profitability given the higher premiums while maintaining a comfortable delta range to minimize risk.

Mid Term Options (Expiring July 19, 2024)

- Strike Prices: $2.5 and $3.0

- Short Put (Sell):

- Strike Price: $2.5

- Delta: -0.0533

- Gamma: 0.1260

- Premium: $0.05

- ROI: 100.0%

- Profit: $0.05

- Long Put (Buy):

- Strike Price: $3.0

- Delta: -0.1316

- Gamma: 0.3457

- Premium: $0.04

- ROI: 100.0%

- Profit: $0.04

This strategy becomes attractive with a $2.5 short put that has a lower delta and gamma, aligning with the goal to stay out-of-the-money. Pairing it with a $3.0 long put offers controlled risk.

Long Term Options (Expiring January 17, 2025)

- Strike Prices: $2.5 and $3.0

- Short Put (Sell):

- Strike Price: $2.5

- Delta: -0.1105

- Gamma: 0.1437

- Premium: $0.05

- ROI: 100.0%

- Profit: $0.05

- Long Put (Buy):

- Strike Price: $3.0

- Delta: -0.2169

- Gamma: 0.2547

- Premium: $0.16

- ROI: 100.0%

- Profit: $0.16

Long-term options with a $2.5 short put and a $3.0 long put provide higher premiums with reduced assignment risk due to moderate delta values.

Very Long Term Options (Expiring January 16, 2026)

- Strike Prices: $2.5 and $3.0

- Short Put (Sell):

- Strike Price: $2.5

- Delta: -0.1453

- Gamma: 0.1175

- Premium: $0.20

- ROI: 100.0%

- Profit: $0.20

- Long Put (Buy):

- Strike Price: $3.0

- Delta: -0.2341

- Gamma: 0.1602

- Premium: $0.40

- ROI: 100.0%

- Profit: $0.40

The $2.5 short put for the longest expiration period offers compelling profitability combined with acceptable risk parameters. This strategy benefits from larger premiums while staying within a tolerable delta range.

Conclusion

When aiming at vertical bull put spread strategies for GRAB, the described combinations of short and long puts across different expiration dates ensure an optimal balance between profitability and risk management. The common thread is choosing slightly out-of-the-money positions to avoid the risk of assignment while capitalizing on favorable premiums and greeks, adapted to fit near-term to very long-term investment horizons.

Vertical Bear Call Spread Option Strategy

A vertical bear call spread is a bearish options strategy where a trader sells a call option at a lower strike price and buys another call option at a higher strike price, both with the same expiration date, expecting the underlying stock price will stay below the strike price of the sold call. In this analysis for Grab Holdings Limited (GRAB), we'll focus on maximizing profitability while mitigating the risk of having shares assigned by selecting suitable expiration dates and strike prices. Each position is crafted considering the delta risk associated with the sold leg being in-the-money (ITM).

Near-Term Choices

- May 2024 Expiration, Strike Prices: Sell $3.0, Buy $3.5

- Sell Call ($3.0)

- Delta: 0.9921

- Premium: $0.58

- Profit Potential: $0.0912

- Buy Call ($3.5)

- Delta: 0.6821

- Premium: $0.15

- Profit Potential: $0.15

With the near-term May expiration, this spread provides good profit potential with an expected decline below the $3.0 mark. The high delta (0.9921) on the sold call indicates a high probability of shares being ITM, thus risk of assignment is notable but offset by the high ROI.

Near-Intermediate Choices

- June 2024 Expiration, Strike Prices: Sell $3.5, Buy $4.0

- Sell Call ($3.5)

- Delta: 0.5859

- Premium: $0.20

- Profit Potential: $0.20

- Buy Call ($4.0)

- Delta: 0.2074

- Premium: $0.04

- Profit Potential: $0.04

For the June expiration, selling a call at the $3.5 strike and buying a call at the $4.0 strike can yield a high return with reduced risk. The delta of 0.5859 is moderate, ensuring that probability of assignment is significantly minimized.

Intermediate Choices

- August 2024 Expiration, Strike Prices: Sell $3.5, Buy $4.0

- Sell Call ($3.5)

- Delta: 0.5940

- Premium: $0.30

- Profit Potential: $0.30

- Buy Call ($4.0)

- Delta: 0.3001

- Premium: $0.10

- Profit Potential: $0.10

By extending to the August expiration, the delta and risk of assignment remain moderate while allowing for a substantial profit. The delta value of the sold call ensures a balanced risk-to-reward ratio.

Long-Term Choices

- October 2024 Expiration, Strike Prices: Sell $3.5, Buy $4.0

- Sell Call ($3.5)

- Delta: 0.6056

- Premium: $0.35

- Profit Potential: $0.35

- Buy Call ($4.0)

- Delta: 0.3968

- Premium: $0.20

- Profit Potential: $0.20

Considering the longer-term expiration in October, selling a call at the $3.5 strike and buying one at $4.0 provides steadiness in terms of risk and reward. The delta of the sold call offers a reasonable expectation of controlling assignment risks over this longer period.

Very Long-Term Choices

- January 2025 Expiration, Strike Prices: Sell $3.5, Buy $4.0

- Sell Call ($3.5)

- Delta: 0.6223

- Premium: $0.52

- Profit Potential: $0.52

- Buy Call ($4.0)

- Delta: 0.4762

- Premium: $0.30

- Profit Potential: $0.30

For the longest-term expiration in January 2025, the same strike spread yields a generous premium. The sold call's delta signifies a moderate risk of assignment, with substantial profitability, indicating a safe yet rewarding spread.

Each of these spreads balances the risk of shares being assigned with profitability, enabling flexibility based on the current stock price and targeted analysis. The deltas of the sold calls are chosen to ensure a controlled level of ITM risk, while the varying expiration dates offer traders a range of probable market scenarios and profit potentials.

Vertical Bull Call Spread Option Strategy

When structuring a vertical bull call spread, it is crucial to carefully select combinations of long and short call options to maximize profitability while managing the risk of having shares assigned. The following analysis based on different expiration dates and strike prices focuses on identifying the most profitable strategies, with an emphasis on reducing the risk of early assignment for options that are in the money (ITM).

Short-Term Strategy (Near Term)

Expiration Date: May 17, 2024 - Short Call: 3.0 Strike (Delta: 0.9921, Premium: $0.58) - Long Call: 2.5 Strike (Delta: 0.9534, Premium: $1.06)

This pair forms a reliable vertical bull call spread as they are close to being in the money while providing a robust profit margin due to their high implied volatility and favorable gamma values. However, the risk of having shares assigned is relatively higher because the short call has a high delta, indicating a strong likelihood of the option ending in the money.

Medium-Term Strategy

Expiration Date: June 21, 2024 - Short Call: 3.0 Strike (Delta: 0.8842, Premium: $0.6) - Long Call: 2.5 Strike (Delta: 0.8495, Premium: $1.35)

This spread provides a balanced risk-reward ratio with delta values suggesting significant movement potential due to the higher gamma. The theta values imply reasonable time decay, and since both options expire soon, the possibility of the trade becoming highly profitable is high while managing the assignment risk effectively.

Expiration Date: July 19, 2024 - Short Call: 3.5 Strike (Delta: 0.5859, Premium: $0.24) - Long Call: 2.5 Strike (Delta: 0.9268, Premium: $1.1)

In this example, the delta difference portrays a clear advantage in terms of time value without having excessive in-the-money risk. It allows for favorable leverage on the stock's movement while maintaining a respectable profit margin with a calculated decrease in the likelihood of early assignment.

Long-Term Strategy

Expiration Date: August 16, 2024 - Short Call: 3.5 Strike (Delta: 0.5940, Premium: $0.3) - Long Call: 3.0 Strike (Delta: 0.7930, Premium: $0.65)

With more time to expiration, this spread leverages both delta and gamma calculations, which signify potential increased profitability while the theta values remain minimal, reducing time decay concerns. The long call strikes a fine balance with the short call, allowing expected increases in the target stock price to capture favorable premiums.

Expiration Date: January 17, 2025 - Short Call: 3.5 Strike (Delta: 0.6223, Premium: $0.52) - Long Call: 2.5 Strike (Delta: 0.8692, Premium: $1.24)

This pairing provides a packed time frame for reaping benefits from bullish movements. The option's delta and gamma behave cohesively, offering the expected progressive increase in the share value. Due to long-term positions, lambda (the long-ranged impact of changes) impacts this strategy positively compared to having a larger risk of assignment in nearer-term spreads.

Extra Long-Term Strategy

Expiration Date: January 16, 2026 - Short Call: 4.0 Strike (Delta: 0.6093, Premium: $0.75) - Long Call: 3.0 Strike (Delta: 0.7582, Premium: $1.15)

This longer-term strategy heavily leans on delta stability and reduced gamma volatility over time, creating a spread that derives profit from steady appreciation in the stock price. The time horizon provides ample flexibility for stock price movements while capitalizing on positive rho coefficients for longer expirations.

By concurrently analyzing delta, gamma, and theta for these paired options per expiry, we mitigate significant assignment risks while leveraging favorable stock movements to optimize profitability. This various-window strategy ensures options fit all trading timelines, prioritizing balance between gain potential and risk exposure due to early assignments.

Spread Option Strategy

When considering the most profitable calendar spread options strategy for Grab Holdings Limited (GRAB), where the goal is to buy a call option and sell a put option, we need to balance the risk/reward ratio while minimizing the likelihood of share assignment. Calendar spreads typically involve options with the same strike price but different expiration dates.

Near-Term Options (Expiration: 2024-06-21)

- Buy Call (Strike: 2.0, Expire: 2024-06-21)

- Greeks: Delta: 0.8659, Gamma: 0.0711, Vega: 0.2416, Theta: -0.0093, Rho: 0.1179

- Premium: 1.51

- Profit: 0.1212

Sell Put (Strike: 2.5, Expire: 2024-06-21) - Greeks: Delta: -0.0837, Gamma: 0.1492, Vega: 0.1719, Theta: -0.0022, Rho: -0.0338 - Premium: 0.10 - Profit: 0.1

This combination provides a good delta exposure for the call option and a neutral-to-bullish outlook, with minimized risk due to relatively low delta for the put option.

Intermediate-Term Options (Expiration: 2024-07-19)

- Buy Call (Strike: 1.5, Expire: 2024-07-19)

- Greeks: Delta: 0.9188, Gamma: 0.0228, Vega: 0.2242, Theta: -0.0078, Rho: 0.0847

- Premium: 1.90

- Profit: 0.2312

Sell Put (Strike: 2.5, Expire: 2024-07-19) - Greeks: Delta: -0.0533, Gamma: 0.1260, Vega: 0.1618, Theta: -0.0007, Rho: -0.0370 - Premium: 0.05 - Profit: 0.05

This pair offers a solid positive delta and higher premium for the call, while the put maintains a low delta, protecting against the risk of assignment.

Mid to Long-Term Options (Expiration: 2024-08-16)

- Buy Call (Strike: 2.0, Expire: 2024-08-16)

- Greeks: Delta: 0.9334, Gamma: 0.0784, Vega: 0.2310, Theta: -0.0014, Rho: 0.4240

- Premium: 1.57

- Profit: 0.0612

Sell Put (Strike: 3.0, Expire: 2024-08-16) - Greeks: Delta: -0.1265, Gamma: 0.3380, Vega: 0.3711, Theta: -0.0006, Rho: -0.1241 - Premium: 0.10 - Profit: 0.1

This spread combines a slightly higher delta call option with a relatively low-risk put, making it a suitable choice for a moderate upward movement.

Long-Term Options (Expiration: 2025-01-17)

- Buy Call (Strike: 1.0, Expire: 2025-01-17)

- Greeks: Delta: 0.9769, Gamma: 0.0187, Vega: 0.1598, Theta: -0.0004, Rho: 0.5753

- Premium: 2.38

- Profit: 0.2512

Sell Put (Strike: 2.0, Expire: 2025-01-17) - Greeks: Delta: -0.0538, Gamma: 0.0704, Vega: 0.3196, Theta: -0.0003, Rho: -0.1576 - Premium: 0.05 - Profit: 0.05

This position emphasizes a lower risk of assignment with the put option, supported by the call's positive delta and reasonable vega exposure.

Very Long-Term Options (Expiration: 2026-01-16)

- Buy Call (Strike: 1.5, Expire: 2026-01-16)

- Greeks: Delta: 0.9391, Gamma: 0.0409, Vega: 0.5545, Theta: -0.0004, Rho: 1.7781

- Premium: 2.10

- Profit: 0.0312

Sell Put (Strike: 2.5, Expire: 2026-01-16) - Greeks: Delta: -0.1453, Gamma: 0.1175, Vega: 1.0502, Theta: -0.0003, Rho: -1.1810 - Premium: 0.20 - Profit: 0.2

The long-term strategy looks to benefit from the higher vega of both the call and put, with the call having a strong positive delta reducing the assignment risk through limited put exposure.

These scenarios offer profitable routes using a calendar spread on GRAB while balancing risk and reward through varied expiration dates and strike prices. Each choice considers the Greeks and the premiums to ensure a sophisticated approach to options trading with minimized risk of having the shares assigned.

Calendar Spread Option Strategy #1

To develop a profitable calendar spread options strategy for Grab Holdings Limited (GRAB), we need to consider both the purchase of a put option and the sale of a call option at different expiration dates. By leveraging "the Greeks," such as delta, gamma, and theta, we can gauge the potential risk and reward. In order to minimize the risk of having shares assigned, we aim to select options that are not deep in the money.

1. Near-Term Calendar Spread (Short Put, Expiring 2024-05-17, Strike 2.5)

For a near-term strategy, consider selling a put option expiring on 2024-05-17 with a strike price of $2.5. This option has a high delta of approximately 0.95, implying a strong probability of being in the money. Although this increases the risk of assignment, its high gamma suggests high sensitivity to underlying price movements, which can be beneficial in volatile market conditions. The ROI of about 6.71 and profit margin align well with the expectations in a short-term scenario where the stock price is expected to fluctuate slightly around the current level. The vega value is relatively low, indicating limited exposure to volatility changes, while the theta suggests a decent time decay in favor of the strategy.

2. Short-Medium Term Calendar Spread (Short Put, Expiring 2024-06-21, Strike 3.5)

In the short to medium-term horizon, selling a put option with an expiration date of 2024-06-21 and a strike price of $3.5 offers a great balance. This option has a delta of around 0.58, representing a moderate probability of expiring in the money, thus reducing the risk of assignment compared to deeper ITM options. It also boasts a high gamma and an excellent ROI of 100.0, indicating high sensitivity and profitability. The theta value supports a controlled time decay effect. Additionally, the high vega suggests that the position is well-hedged against volatility changes.

3. Medium-Term Calendar Spread (Short Put, Expiring 2024-07-19, Strike 3.0)

For a medium-term strategy, selling a put option expiring on 2024-07-19 with a strike price of $3.0 is feasible. This option exhibits a delta of approximately 0.82, balancing the risk of assignment while maintaining significant price sensitivity (evidenced by its gamma). The vega and theta values align well with maintaining stability in volatility and time decay, respectively. The ROI of around 24.8 indicates a fairly high return. Coupled with sufficient profit margins, this option can be quite lucrative if the stock price remains within 2% of its current value.

4. Long-Medium Term Calendar Spread (Short Put, Expiring 2024-09-20, Strike 3.5)

In a longer medium-term setup, consider selling a put option with a strike price of $3.5 expiring on 2024-09-20. The delta of around 0.60 strikes a fine balance between a moderate risk of assignment and potential profitability. This option's high gamma and substantial vega indicate its strong response to price changes and exposure to volatility, augmenting its profit potential. An ROI of 100.0 and favorable theta further support the profitability of this trade over an extended period.

5. Long-Term Calendar Spread (Short Put, Expiring 2026-01-16, Strike 3.0)

Finally, for a long-term strategy, selling a put option with a strike price of $3.0 expiring on 2026-01-16 could be extremely beneficial. This option carries a delta of approximately 0.76, which presents a fine balance between minimizing the risk of assignment and optimizing return potential. The gamma value and the exceptionally high vega underscore the option's responsiveness to price movements and volatility. The theta supports manageable time decay, while the ROI of 57.5 and substantial profit margins offer an attractive long-term investment opportunity.

In conclusion, a calendar spread strategy involving buying a long call option and selling an optimized put option with carefully selected expiration dates and strike prices can yield profitable results for GRAB. Each of these five strategies balances risk and reward by leveraging delta, gamma, theta, and vega to ensure favorable outcomes while minimizing the chances of share assignment.

Calendar Spread Option Strategy #2

To devise a profitable calendar spread options strategy that minimizes the risk of having shares assigned, we need to select options that are one strike price slightly in or around the money for the put and the call, considering the target stock price range of 2% over or under the current stock price. This will help us capture the most significant time decay benefits from the sold put option while maintaining the potential for profit from the purchased call option at a later expiration date.

-

Near-Term Strategy (May 17, 2024 Expiration) Sell: A put option with an expiration date of May 17, 2024, strike price $2.0 (delta approximately 0.988). Despite its high delta, indicating it's deep in the money, the short duration makes assignment risk moderate. Buy: Since there is no data for long calls in the tables, consider buying a call option with an expiration that aligns with a subsequent bearish sentiment timeframe within the year but still leverages the bearish assumption made in the near stock price.

-

Medium-Term Strategy (June 21, 2024 Expiration) Sell: A put option expiring on June 21, 2024, with a strike price of $2.5 (delta approximately 0.849). This position is closer to being in the money but bears a higher delta, meaning it is somewhat safer regarding assignment risk due to a lower delta compared to the near-term strategies. Buy: A long call option extending beyond June, considering the seasonal or quarterly performance peaks of the company, potentially targeting expiration dates in September.

-